Bubble or Boom?-What History Suggests

Bubble or Boom?-What History Suggests

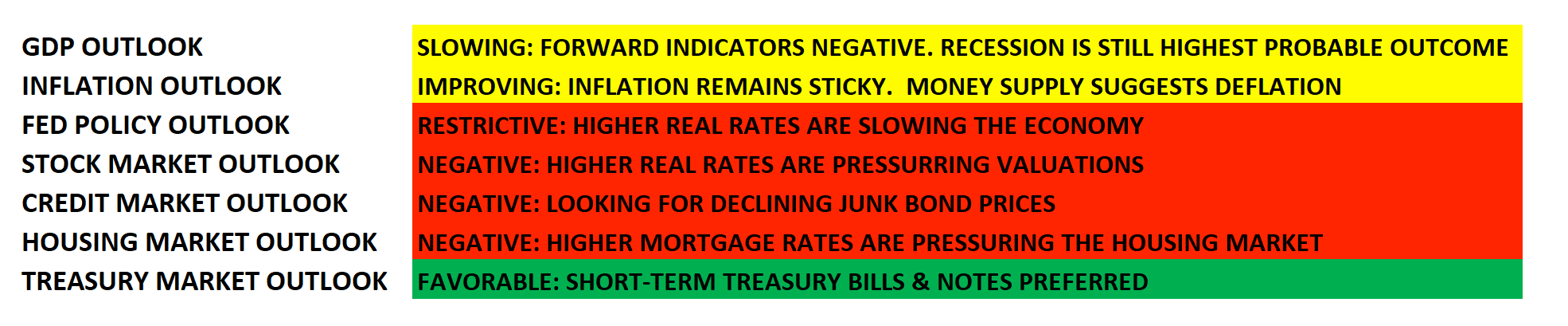

LHWM Market Quick View-October 2023

Key Take Away

Recessionary leading economic signals remain, yet the market has bounced in November. But why? The largest influence has been liquidity driven by the Treasury. At the end of July, the Treasury massively increased the amount of long-term bonds issued due to the massive government deficit. That marked the top of the July stock rally as long-term yields rose 100 basis points in the following months as stocks fell 10%. Then, likely due to a bit of panic from the August - October market reaction, the Treasury surprised investors by increasing the amount of short-term treasuries vs long-term bonds to be issued in the quarter ahead. As a result, long-term yields have declined by 50 basis points, and stocks have rallied 10%. Meanwhile, the budget deficit remains; the government just opted to meet its funding needs with increased short-term financing to take pressure off long-term rates. The can has been kicked down the road again, for now. After all, 2024 is an election year, and no matter which party is the incumbent, all tactics will be used to push any chances of a recession at the expense of our longer-term success.

This recent stock market bounce has further exacerbated the performance between the market-cap-weighted S&P 500 and the equal-weighted S&P 500 to record levels of disparity. With the Magnificent Seven stocks pushing the pile for the overall market (now accounting for nearly 30% of the value of the market cap-weighted S&P 500), the rest of the market has yet to participate in a material rebound. The bubble in mega-cap tech stocks remains intact, but so does the higher-than-average risk of a global recession. There is mounting evidence that a recession is very near; however, recession or not, we believe the truth will reveal itself over the coming quarters.

With history as our guide, we’ve seen this type of speculative bubble before. Eventually, they do pop… and usually in spectacular fashion. Timing is always a challenge, but gravity is still an undisputed force.

U.S. Outlook (Next 3-12 Months)

Overview

“The Nifty Fifty appeared to rise up from the ocean; it was as though all of the U.S. but Nebraska had sunk into the sea. The two-tier market really consisted of one tier and a lot of rubble down below. What held the Nifty Fifty up? The same thing that held up tulip bulb prices long ago in Holland – popular delusions and the madness of crowds. The delusion was that these companies were so good that it didn’t matter what you paid for them; their inexorable growth would bail you out.”-Dr. Hussman

– Forbes Magazine, 1977, The Nifty Fifty Revisited

The more things change, the more they stay the same. One of the research firms we follow is Hussman Strategic Advisors. In their November market commentary(https://www.hussmanfunds.com/comment/mc231120/), Dr. Hussman highlighted the above quote as a reminder that we have been here before. The Nifty 50 from the early 70’s and the Glamour Tech stocks from the ‘99/’00 are just two more recent examples. In both instances, investors fell in love with a group of stocks that seemingly only went up and could do no wrong. It's eerily reminiscent of the Magnificent Seven Stocks today or the stock and housing market before the 1929 depression. Both prior events were ultimately speculative bubbles that ended with crashes where the previously beloved stocks declined between 50% - 80%.

Hussman points out that when it comes to the current Mega-cap Growth stocks, investors forget that growth rates and operating margins tend to decline as companies dominate. When a young company grows its business annually at a high percentage rate, its stock is rewarded with a high valuation. As time progresses and growth is achieved, the growth rate begins to slow. Eventually, the company has grown so much over the years that it dominates its industry, and growth prospects continue to slow. When a young company is growing rapidly, there is an opportunity for the company to grow into a high valuation thanks to the rapid growth rate, so depending on the economic conditions, paying too much may still yield generous returns. As a company matures and growth slows, the opportunity for the company to grow into an overpriced stock valuation becomes far more difficult especially when the global economy slows. “The greatest danger emerges when valuations are rich despite relatively low growth, making it particularly difficult to grow out of errors. My impression is that investors are likely to learn this lesson from some very, very large companies, not to mention the S&P 500 itself.”-Dr. Hussman

We remain patient, waiting for data and indicators to provide reasons to be more bullish or fundamentally optimistic about stocks going into 2024. We are watching for improvements in the Leading Economic Index, for signs of lower inflation (and thus interest rates) without a recession, an acceleration in global manufacturing, an increase in productivity, and broader stock market sector participation. When these things show improvement and our indicators confirm, we will increase equity exposure and invest for longer-term growth. Until then, the smart money plays defense. The current economic conditions align most with the type of conditions that have preceded troubled stock market returns vs bonds, at least historically speaking.

Model Positioning

Short-term treasury notes continue to be the largest portfolio holding. We have recently been able to use proceeds from maturing 12-month notes purchased last year to buy new 24-month notes with yields of just over 5%. From our perspective, this remains the best risk-adjusted investment opportunity as we wait for a brighter economic setup.

Portfolio models continue to be underweight equity exposure, with holdings in defensive value/dividend-oriented funds. Last month, we mentioned that the technical backdrop for the market appeared to be setting up for a potential short-term bounce. It turns out our suspicions were correct; the market has since bounced. At this point, we believe the market no longer appears oversold in the near term; the bounce has already gone too far, too fast. Speculation is far from dead.

Eventually, we will get more aggressive with portfolio allocations. It is best (risk-reward ratio) to invest for growth when the economic wind is at your back. Our main thesis remains that recession odds are high, and the Federal Reserve is likely to hold rates high until something breaks in the financial sector, the stock market breaks, or we have a miraculous soft landing (slow growth, low inflation without a recession). The longer rates remain high, the more susceptible stocks will be to repricing lower. Unfortunately, it takes some time for things to play out in the global economy...the Titanic turns slow. We expect the market to remain volatile as long as economic growth remains weak and inflation remains high. To navigate this volatility, we will continue to adjust exposures (long and short) based on macroeconomic and market indicators to reduce portfolio volatility and protect capital. Economic risks remain elevated, and thus, we remain cautious.

Keys to the Market

S&P 500 Forward PE – Currently, market multiples on stocks are not cheap. According to Hussman Strategic Advisors, “given the popularity of the S&P 500 price / forward operating earnings ratio – a measure that only became popular in the 1990s, it’s worth understanding that a forward P/E (price to earnings ratio) of 20 is not cheap by any stretch of the imagination. While the forward P/E is based on the future earnings estimates of Wall Street analysts, and the Shiller cyclically-adjusted P/E (CAPE) is based on the 10-year smoothing of past reported earnings, there is a strong enough relationship that we can overlay the two to get a sense of what a historically “normal” forward P/E would be. That norm is close to 11.”-Dr. Hussman

*Source: Hussman Strategic Advisors

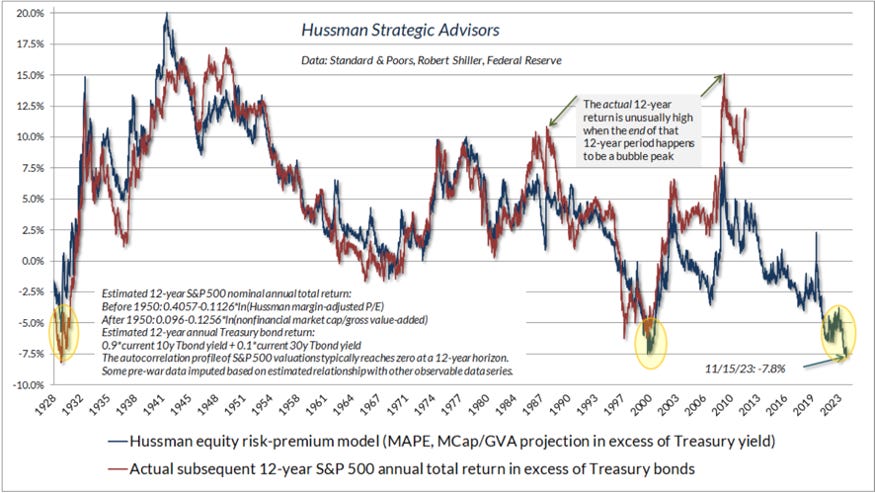

Forward Expected Returns – Given current stock valuations and interest rates, forward expected returns on stocks from current levels are essentially zero. From Hussman Strategic Advisors: “The chart below shows our estimate of likely 12-year S&P 500 total returns, over-and-above the return available on Treasury bonds. I show this chart because the current estimate, at -7.8%, is the worst level in history. It’s true that if the end of a 12-year investment horizon happens to be a bubble peak, actual returns (red) might peel away from our estimates (blue). Yet even then, the worst “error” resulting from end-of-horizon bubble valuations has been about 7.5%. Given that we expect a -7.8% gap (with the S&P 500 losing value over a 12-year horizon while bonds earn positive returns), even a 7.5% error would put stock returns behind bonds. Not that we view bond yields as quite “adequate” either, but I do believe that most of the bond market losses are behind us. Stocks are another matter entirely. That’s what you get after more than a decade of Fed-driven yield-seeking speculation.”-Dr. Hussman

*Source: Hussman Strategic Advisors

“The chart below shows the same data in a different way. The yellow bubbles show points when our estimates of S&P 500 total returns were below prevailing 10-year Treasury yields. The 1929, 1968, 1998, and 2007 instances were indeed followed by very long periods of lagging S&P 500 performance relative to bonds. I don’t expect the current instance to be different.” -Dr. Hussman

*Source: Hussman Strategic Advisors

Performance Gap – Per Hussman: “The chart below shows what’s been going on internally. Notice that the S&P 500, weighting its components by market capitalization, has clearly outperformed the same S&P 500 components, equally weighted. The capitalization-weighted S&P 500 has also outpaced the NYSE Composite and the Russell 2000, as well as stocks characterized by “value” factors. This unusual gap largely reflects narrow attention by investors on stocks dubbed as the “Magnificent Seven”: Apple, Microsoft, Alphabet, Amazon, Meta, NVIDIA, and Tesla.”-Dr. Hussman

While the stock market remains richly valued and the risk of recession remains elevated, LHWM portfolios remain defensively allocated. While we believe the risk/reward and outlook for stocks is currently poor, an eventual drop in stock prices, offering a lower entry point, is an opportunity we patiently await. Soon, we believe the truth about the state of the economy and market will be revealed.

Our goal is to help you grow your wealth over time while managing the risk of significant drawdowns along the way. After all, the worst outcome for our clients is to have “made it” yet lose or greatly reduce the ability to maintain financial independence due to poor risk management during economic recessions. Markets never go in a straight line. As we remain defensive, awaiting indication from our technical and economic signals for the time to get bullish, patience is needed to ride out the storm. We remain vigilant in navigating these uncertain markets and searching for the start of the next meaningful uptrend. During the course of our relationship, we have worked with you to establish a portfolio that matches your financial planning needs, risk tolerance, and investment timeline. It is critical to remain patiently invested in the appropriate model. Stick to the plan!

Please do not hesitate to contact us with any questions, comments, or to schedule a portfolio review.

Sincerely,

Lake Hills Wealth Management