Housing Headwinds

Key Take Away

Real estate is a key leading sector for the overall economy. In past recessions, real estate has often led the economy down and been one of the first sectors to rebound, leading the economy out of recession. The combination of high housing prices and the onset of sudden, high mortgage rates has caused real estate activity to slow over the last 12 months. Despite the slowness and modest softening of housing prices so far, home affordability remains near historic lows. Some significant combination of lower housing prices, lower interest rates, and or higher wages is desperately needed to get housing affordability back to historical average levels.

Lake Hills models continue to be defensively positioned while pursuing a barbell approach with portfolio construction to navigate the dueling possibilities of recession and soft landing (albeit a lower probability outcome).

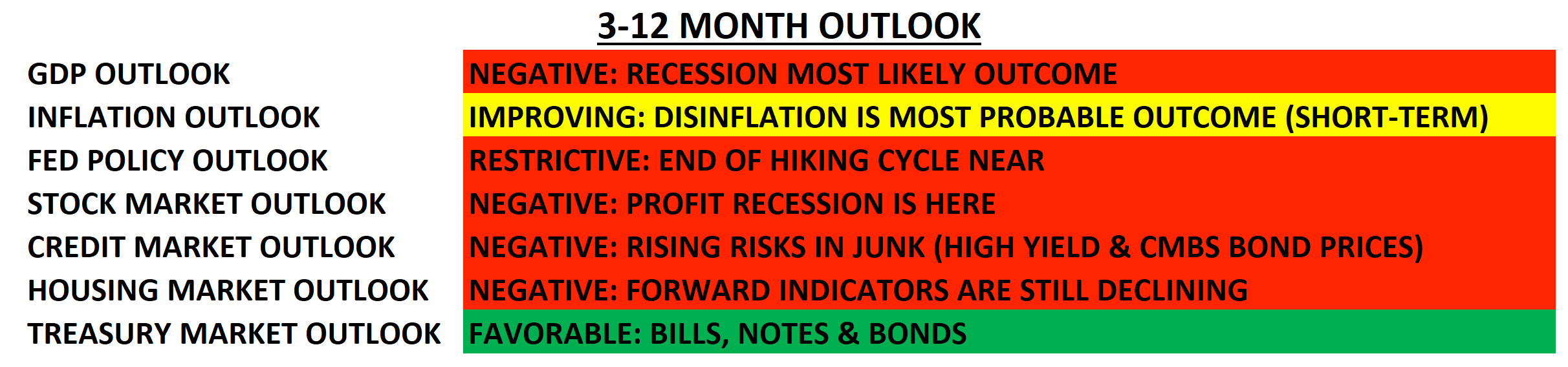

U.S. Outlook (Next 3-12 Months)

Overview

The assumption that home prices only go up was the flawed assumption of the early 2000s that led to excessive risk-taking in real estate and ultimately led to the Great Financial Crisis of 2008 that nearly brought the world to its knees as major financial institutions collapsed. The housing bubble that peaked in 2006 was a byproduct of excess liquidity, relaxed regulation, declining interest rates, and excessive risk-taking.

Individuals and investors were borrowing as much as they could to buy houses they couldn’t afford with hopes of making a quick buck. It was not uncommon for someone to own multiple houses they couldn’t afford, with the idea being they could rent the houses out or flip them for a profit after a short holding period. The Federal Reserve continued to lower interest rates during the 2000s as CPI inflation was low. This just added fuel to the fire. As mortgage rates decrease, borrowers can afford more expensive houses without any increase in income. Rate cuts are a major tailwind for housing prices, as with almost all risk assets as well. Wall Street mades a fortune by making it easy for buyers to access money without having to prove they had the resources to pay the mortgage...remember the NINJA (No Income, No Job, and no Assets) loans? When it comes to investing, the market is in constant flux between fear and greed, which often makes market participants do the opposite of what is prudent.

“You can’t stand to see your neighbor getting rich. You know you’re smarter than he is, and he’s doing these things, and he’s getting rich".”-Warren Buffett.

The real estate frenzy of the early 2000s continued until housing affordability reached highs that began to price buyers out of the market. Consumers were becoming overextended, and real estate began to slow. It took two years for the bubble to really burst when the 2008 recession finally hit. Housing prices proceeded to decline for several years (until 2012), returning housing affordability to more historical levels (see charts below).

After the 2008 financial crisis, the FED began reducing interest rates again, helping the housing market to eventually stabilize and start to rebound as consumers took time to repair their balance sheets. Prior to 2020, housing had rebounded while home prices relative to median income remained well below the 2006 peak…housing was still relatively affordable, at least compared to the 2000s housing bubble. Then Covid arrived, bringing the perfect storm to reaccelerate housing.

Once Covid hit, the response on multiple fronts caused housing prices to soar. First, the FED aggressively cut short-term interest rates to zero and began buying bonds and mortgage bonds, causing 30-year mortgage rates to fall below 3%. This was an enormous boost to housing affordability. Suddenly, buyers could afford more expensive houses without any impact on their budgets. Simultaneously, people wanted to move out of the cities to distance themselves from others, while many could work from anywhere as remote work became prevalent. Renters also wanted more space and amenities as they were going to be stuck working and schooling from home. The work-from-home movement allowed people to move much further away from the office than ever before. From there, the bidding wars commenced, and housing prices rocketed higher. Historically, when liquidity is plentiful and interest rates are artificially low, euphoric speculation erupts.

Additionally, thanks to Covid, as things began to reopen, people were excited to travel again. However, they weren’t eager to go back to hotels and be around lots of people. Thus, short-term rentals (Airbnb) began to boom. Rates remained low, and many began to buy second and third homes to rent out. This put additional strain on supply and demand dynamics as new home construction was due to supply chain challenges, which pushed home prices, and subsequently rents, up.

What happens to housing from here? Many factors that contributed to the substantial increase in housing prices over the last three years have completely changed. We went from 2.8% mortgage rates to above 7% within a 20-month timeframe. Housing prices have not corrected enough, given the high interest rates, to bring affordability down. Core Inflation remains stubbornly high (about double the Federal Reserve Bank’s 2% target), which suggests the FED will not be cutting interest rates any time soon unless a recession hits and/or something systemic breaks. Consumers are becoming stretched as incomes have not kept up with cost of living increases in the past two years, and student loan payments start in October.

Further complicating housing, 2021 supply constraints exacerbated by the boom in short-term rentals could start to unwind. Profitability on rental properties has been recently under pressure. In most markets, it currently costs more to buy than to rent, which brings fewer rental property investors to the market. A number of prior investors are seeing a significant slowdown in short-term rental income, and local governments have turned against the short-term rental market, turning these properties into negative cash flow investments that could soon find themselves for sale. The city of Austin alone has estimated that there are over 11,000 short-term rentals in Austin. If the consumer remains challenged and a hard recession develops, as we forecast, home prices could be under significant pressure. What was a housing supply shortage can quickly change as more short-term rental properties go up for sale just as multi-family properties under construction reach an all-time high (see the chart below).

The outlook for housing remains weak. Drastic adjustments to interest rates, housing prices, or incomes are needed to bring housing affordability back to historical averages. Changes in these dynamics tend to take time, more time than most think. We would not be surprised to see housing prices remain under pressure for several years or longer before stabilizing. Variables can change, and forecasting the future with any accuracy is difficult, however, we believe caution is warranted. If you’re in the market for a home (primary or rental), be patient, do your homework, and be prepared. The best investing opportunities often come when you don’t FEEL like buying, and from our work, that condition isn’t present today.

Model Positioning

We have been pursuing a barbell approach with portfolio construction for the past several months to account for the dueling possibilities of recession and soft landing. On the one hand, portfolios remain defensive and prepared for recession with reduced exposure to equities and significant allocation to short-term treasury notes. During August, the first of the 12-month treasury notes we purchased last year matured. When we started buying treasury notes in 2023, the 12-month yield was around 4.5%. Since then, interest rates have continued to climb. Today, a 12-month note yields just over 5.4%, and we can now buy 24-month notes with a yield of just over 5%. This continues to be the best risk-adjusted investment opportunity as we wait for a brighter economic setup.

For the possibility of a soft landing (no recession), we have added to cyclical stock exposures that should have a significant upside if the economy reaccelerates. Energy stocks have had a tremendous run over the last few months and continue to be one of our favorite equity sectors. Although, for now, even energy stocks are looking a little over-bought. We are taking a trading approach with cyclical exposure. Adding positions that have attractive entry points given recent market technicals. New positions are added with stop loss targets in mind. If the position goes down, we’ll sell to keep losses small, then re-evaluate. If the positions go up, we can ride the gains until momentum wains, adjusting our stop targets upward. Eventually, when the Leading Economic Indicators improve, we can allow these cyclical positions more room to wiggle. For now, our indicators suggest a recession is the highest probability, and the U.S. stock market is historically expensive, so being short-term and cautious is warranted. Preserving wealth should always come before growing wealth.

We expect the market to remain susceptible to bouts of volatility as long as economic growth remains weak and rates and inflation remain high. To navigate this volatility, we will adjust exposures (long and short) based on macroeconomic and market indicators to reduce portfolio volatility and protect capital. Market risk remains elevated, and we remain cautious.

Keys to the Market

Home Price to Median Household Income Ratio – The following chart compares the median income in the U.S. to the average cost of a house. Currently this ratio stands at 7.75. Meaning the average cost of a house is 7.75 times the median U.S. income. By this measure, housing is more expensive now than at any time in the last 75 years.

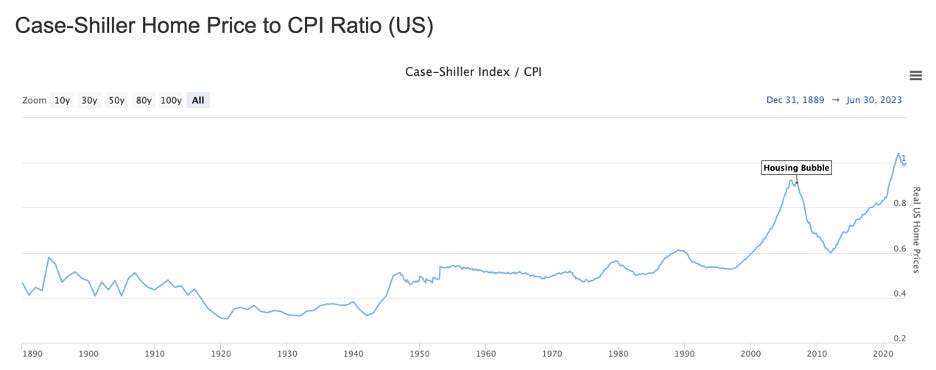

Home Price to CPI Ratio – Home price inflation remained relatively in line with CPI (Consumer Price Inflation) up until the year 2000. What changed? Answer: interest rates. When interest rates declined in the past (articifically low due to Fed), housing prices increased at a faster pace than CPI (early 2000s housing bubble and 2020). When interest rates increased in the past, housing prices stagnated relative to CPI (early 1980s and 1990s). We have recently experienced a significant increase in mortgage rates, and as a result, housing prices have started to slow.

Mortgage Rates – In response to the ’01-’02 recession, the FED began aggressively cutting interest rates to stimulate the economy. As interest rates declined over the following 20 years, housing prices soared. Lower rates allow borrowers to afford more expensive houses. Rates had been steadily falling until 2022. Today, rates are at levels not seen since the year 2000. Housing is an interest-rate-sensitive asset; changes in mortgage rates normally will change the direction of prices with a lag. This price correction is starting for commercial real estate but not yet for residential real estate.

Housing Affordability (part 2) – Initially, the plunge in interest rates in 2020 drastically improved housing affordability. As a result, housing prices then experienced a significant increase the following year, bring affordability back down. Then, with the rapid increase in rates over the last 12 months, housing affordability has plunged to lows not seen since the early 1980s. The combination of high prices and high interest rates has knocked affordability down. According to the Nation Association of Realtors, only 23% of homes listed for sale in the U.S. are affordable for middle-income households or households with annual earnings of up to $75,000.

https://www.cbsnews.com/news/home-prices-housing-affordable-homes/

We are determined to help you navigate this uncertain economic environment with our eyes steadily focused on the warning signs around us. Our goal is to help grow your wealth over time while managing the risk of significant drawdowns along the way. Markets never go in a straight line. As we remain defensive, awaiting indication from our technical and economic signals for the time to get bullish, patience is needed to ride out the storm. We remain vigilant in navigating these uncertain markets and searching for the start of the next meaningful uptrend in the stock market. During the course of our relationship, we have worked with you to establish a portfolio that matches your financial planning needs, risk tolerance, and investment timeline. It is critical to remain patiently invested in the appropriate model. Stick to the plan!

Please do not hesitate to contact us with any questions, comments, or to schedule a portfolio review.

Sincerely,

Lake Hills Wealth Management