Pain Means No Gains for Stocks

Pain Means No Gains for Stocks

LHWM Market Quick View-September 2022

Key Take Away

The reality of policy headwinds and slowing economic data continues to weigh on markets. The July/August stock market rally rolled over and went right off the proverbial cliff after FED Chairman Jerome Powell delivered an extremely hawkish speech on August 25th. He reaffirmed that the FED is steadfast in fighting inflation while acknowledging that “pain” lies ahead for the economy. The following quote from his speech sums it up nicely (emphasis added):

“While higher interest rates, slower growth, and softer labor market conditions will bring down inflation, they will also bring some pain to households and businesses. These are the unfortunate costs of reducing inflation. But a failure to restore price stability would mean far greater pain”. Source: Bloomberg

In other words, they intend to keep rates elevated to make sure that inflation comes down with the understanding that the economy and job market (thus stocks as well) are going to suffer in the process. He also points out the risk of not getting inflation down now would lead to “far greater pain.” So, don’t expect the FED to shift gears and rescue the stock market immediately. Just as they were late to the inflation fight, they will likely be late when it comes time to ease financial conditions to avoid a recession. LHWM models have remained defensively positioned since February.

U.S. Outlook

Overview

We continue to believe the U.S. economy is heading for recession with several consecutive quarters of negative growth headwinds ahead. The FED, continuing to hike rates into this slowing environment, will exacerbate the slowdown. As mentioned above, the FED is committed to fighting inflation and believes rates need to stay higher for longer to knock inflation down. Without saying it explicitly, the FED is telling us a recession is coming to bring inflation down. After all, every recession in U.S. history has brought inflation down.

We’ve highlighted several economic data points in recent months. Here is a quick update on a few of those:

· ISM Manufacturing PMI Survey was at 56.1 in May and is down to 52.8 as of the August reading – readings below 50 signal a contraction.

· High-yield corporate spreads have increased to 522 basis points from 408 in our June update indicating credit markets continue to tighten. This means borrowing conditions have continued to worsen.

· Consumer Sentiment reading came in at 58.2 for August, up from the low reading of 50.0 in June but still far lower than the January reading of 67.2. The July stock market bounce was a likely driver of this improvement. However, sentiment readings this low have only previously been seen in recessions (i.e., 2008 & 1980).

· New Home Sales Volumes have now declined 53% from the post covid peak. As of July, the decline was at 43%. Significant further deterioration.

As one can see, there has been no real improvement to speak of with leading economic data. Additionally, corporate earnings declines have been on our radar for some time now. According to Standard & Poor’s, S&P 500 operating earnings through Q2 2022 have now declined 17% year to date. Wall Street consensus estimates for earnings in 2023 remain elevated at around $243 per share (down from $250). Q2 2022 operating earnings came in at $47.25 per share, which annualizes to $189. If Q2 earnings and our forward earnings models are an indication of what’s to come, then estimates remain WAY too high. Likewise, if earnings disappoint expectations, then stocks are currently far more expensive than most investors realize from a valuation standpoint. Source: Bloomberg

Model Positioning

LHWM model portfolios remain defensive. Stock exposures are virtually unchanged since July and continue to be entirely focused on defensive positions (utilities, high-dividend (lower volatility) stocks, & consumer staples). Similarly, allocations to short equity positions remain in place (these do well when the stock market drops). The biggest portfolio change, as of late, is the accumulation of long-term treasury bonds in the models.

Historically, long-term treasury bonds perform well when the U.S. economy is heading into a recession. Remember, recessions cause inflation and interest rates to go down, which causes bond prices to rise. We believe the economy is headed for recession, and this recession has the potential to be deep. This, coupled with the fact that bonds are currently “out of favor” as they have been declining since July of 2020, makes for a very attractive risk/reward setup. We believe there is now far more upside potential than downside risk but acknowledge we have been early or wrong on this call so far.

We’d also like to point out that the “out of favor” sentiment for bonds can turn on a dime. Interestingly, there are a lot of similarities to the bond market of 2022 and 1987. This year the 10-year treasury yield started out at 1.34% and is now at 3.34%...this equates to a loss of about 20% from a bond price perspective for a 10-year treasury note. In 1987 the 10-year treasury yield went from 7.08% in January up to a peak of 10.23% in October, a loss of around 30% on the price. The FED was raising rates in 1987, and bonds were “out of favor” with investors. Sound familiar? The 1987 peak in rates occurred on October 15th, a Thursday. The bond market was closed on the 16th and did not re-open until Monday the 19th… “Black Monday” when the S&P 500 lost over 20% in a single day. As stocks got pummeled, bonds quickly roared back into favor. From there, yields plummeted, dropping from 10.23% on the 10-year treasury down to 8.97% in just three trading days, a price gain of about 12%. The 10-year yield continued to fall for the following four months generating a gain for investors of approximately 21%. Source: Bloomberg

Of course, we cannot predict a “Black Monday” for the stock market, but we do believe a significant downside remains. If investor sentiment turns in favor of bonds, it could happen very quickly. However, if we are wrong, and the prices of long-term treasury bonds break the lower bound of our price threshold, we may have to sell or trim these positions and wait for another buying opportunity.

Keys to the Market

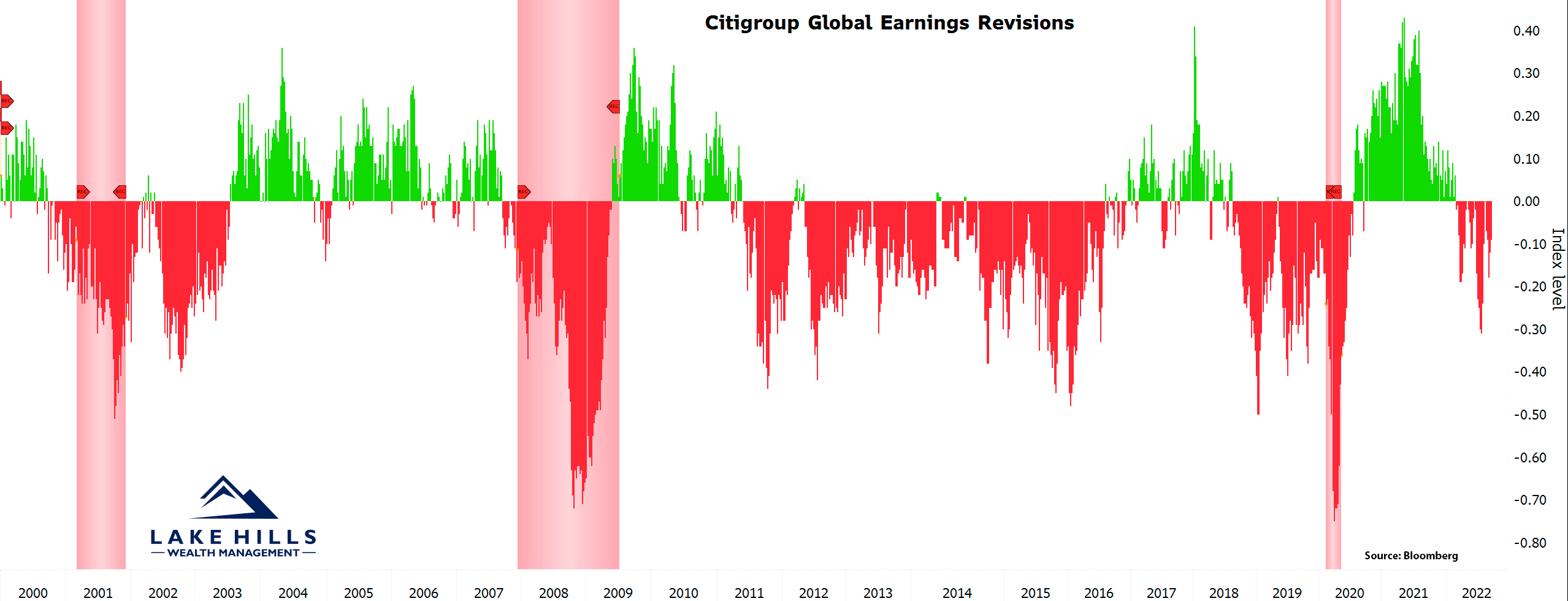

Earnings Revisions – Global earnings revisions have turned negative. We continue to point out that earnings expectations are very high and that earnings disappointment is very likely. Negative earnings revisions are likely to accelerate if the economy indeed goes into recession. Source: Bloomberg

*Red shaded areas indicate NBER-defined U.S. Recession

Rule of 20 – Adding the average PE Ratio (Price to Earnings Ratio) of the S&P 500 to CPI is one way to measure how expensive or cheap stocks are while factoring in inflation. Higher inflation generally demands lower PE ratios, while lower inflation begets higher PE ratios. The higher the PE ratio, the more elevated the stock market will be relative to the earnings. We are coming out of a period of low inflation and high PE ratios and are now in a period of high inflation, which is causing PE ratios to move lower (stock market down). In the past, the S&P 500 has never bottomed with this ratio above 20. As it currently stands, this measure still sits at 27.5 (PE of 19 + CPI of 8.5%). Source: Bloomberg/Bank of America

*Red shaded areas indicate NBER-defined U.S. Recession

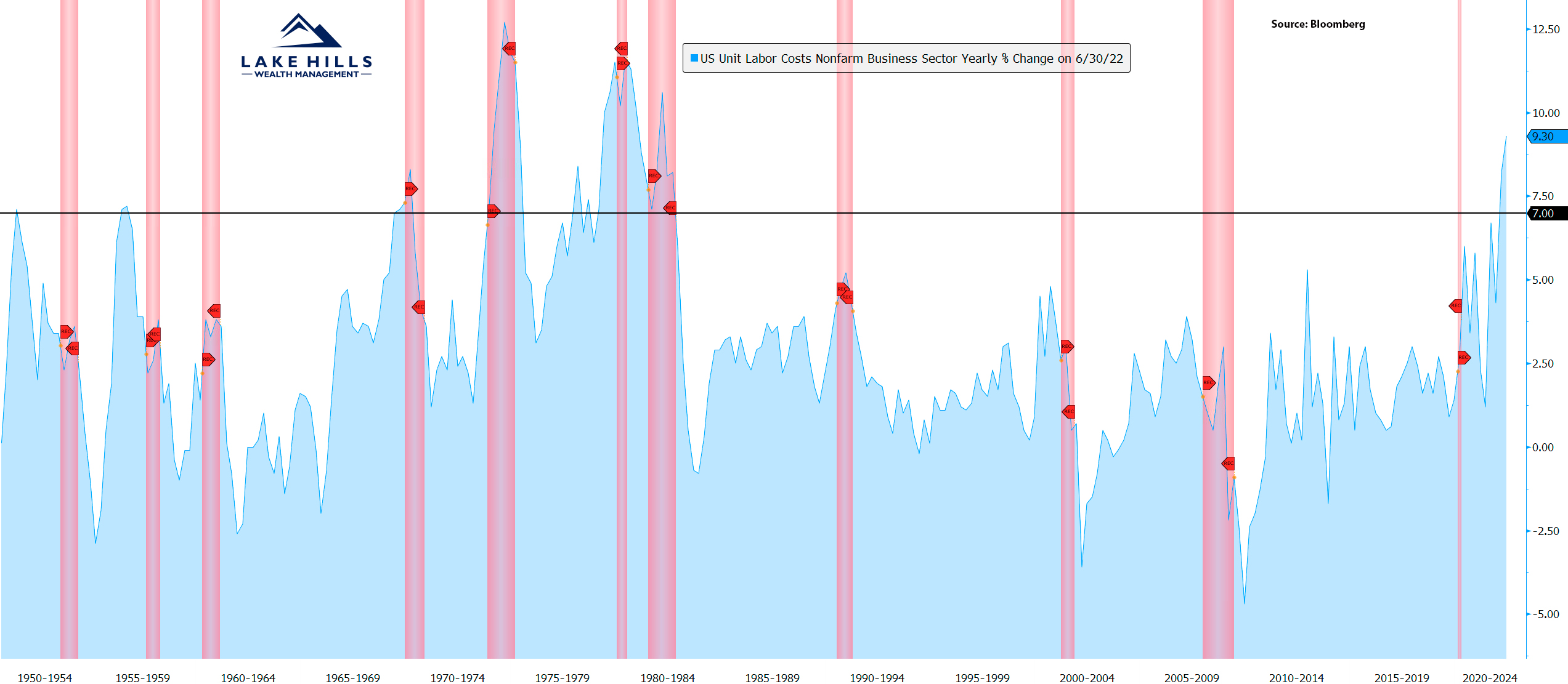

Unit Labor Costs – Unit labor costs have risen sharply in 2022. This is a measure of the cost of labor that businesses pay to produce a unit of output across the economy. Rises in labor costs are highly correlated to recessions. As labor costs increase across the economy, profits drop. Falling profits cause companies to reduce expenses (including layoffs) which contributes to the recessionary forces that eventually cause the unit labor costs to once again decline. Source: Bloomberg

*Red shaded areas indicate NBER-defined U.S. Recession

Bear markets and recessions take time to unfold. The most difficult aspect of a bear market is to remain defensive while risk remains high. However, with a little patience, we believe this downturn will bring great opportunity for investment. We remain conservatively positioned and vigilant in navigating these uncertain markets. We have worked with you to establish a portfolio that matches your financial planning needs, risk tolerance, and investment timeline. As always, it’s critical to stay invested in the appropriate model and stick to the plan.

Please do not hesitate to contact us with any questions, comments, or to schedule a portfolio review.

Sincerely,

Lake Hills Wealth Management