Patience & Flexibility Required

Patience & Flexibility Required

LHWM Market Quick View-December 2023

Key Take Away

In portfolio construction, flexibility is essential for success. It is imperative to navigate market and economic changes, effectively, enabling the removal of underperforming assets and seizing new opportunities. While identifying winning investments involves a meticulous process, adapting to market dynamics requires swift action.

Persistent recession indicators, unprecedented economic uncertainties, narrow market leadership, and bubble valuations have been the driving force for reduced equity exposure across portfolio models. Reduced stock exposure during periods of heightened risk is integral to our strategy. As we have seen, recessions take time to materialize and just because they haven’t yet happened doesn’t make the risk go away. Observing recent trends, such as governmental initiatives aimed at stimulating economic growth and stabilizing financial markets, has promoted optimism for a potential economic resurgence. Recent upticks in U.S. manufacturing new orders hint at the possibility of real economic green shoots. While a significant risk of a global recession remains (Japan and parts of Europe look to be in a recession now), we stress the fact that there are no certainties in global finance or life in general.

As we await evidence of a recession or a reacceleration of growth and inflation, market signals play a crucial role in assessing risk sentiment. Despite lingering recession concerns, current stock market indicators favor continued upward momentum albeit the risk/reward looks poor at least for long-term investment decisions. While short-term technical indicators suggest a correction for the euphoric overbought market, prompting caution in the near term. A pullback in stock prices over the next month or so could provide an opportunity to “buy the dip,” barring any material changes, in the areas of the market that we believe offer a better risk/reward profile and higher income.

Navigating today's market requires adaptability and lots of patience. While we believe maintaining a defensive tilt in portfolio allocations is prudent, we remain vigilant for opportunities as market conditions evolve. Flexibility is essential in seizing opportunities and mitigating risks in what looks like another stock market bubble.

U.S. Outlook (Next 3-12 Months)

Overview

When it comes to our health, extensive research has highlighted the significant benefits of incorporating stretching and flexibility exercises into our routines. Not only do they enhance physical performance, but they also mitigate the risk of injury by expanding our range of motion and optimizing blood circulation, enabling muscles to function more efficiently.

Similarly, in the realm of portfolio construction, fostering flexibility and having a sound process is paramount for long-term success. Although it may pose challenges, maintaining agility with portfolio holdings empowers us to weed out underperformers and seize new investment opportunities. Just as identifying winning investments is a meticulous process guided by predefined criteria, adapting to market dynamics demands swift action. Sometimes, a new position yields immediate success, validating our initial investment rationale. Yet, on other occasions, despite meeting favorable conditions initially, a position may unexpectedly falter, necessitating its removal from the portfolio.

The ultimate objective, through this dynamic process, is to cultivate a portfolio of robust positions, capitalizing on winners while swiftly cutting losses to make room for fresh opportunities. Although managing risks can prove daunting, especially amidst prevailing economic uncertainties, it is integral to our strategy for protecting wealth. Observing persistent recession indicators signaling caution for over a year and a half, our approach entails heeding these warnings and adjusting portfolio exposure during periods of heightened risk.

While recessions often manifest gradually, their implications are profound, particularly in election years, prompting policymakers to deploy various measures to stimulate economic growth and stabilize financial markets. Observing recent trends, governmental initiatives have aimed at reducing long-term bond supply (while greatly increasing short-term treasury issuance) to ease pressure on liquidity and long-term interest rates while fostering rate cut expectations through the Federal Reserve's nuanced communication on interest rates and inflation. This has cultivated increased optimism for a potential soft landing, lower growth, and inflation without large job losses which looking historically, has only happened about 20% of the time.

Moreover, amid ongoing vigilance regarding recession indicators, we remain attentive to leading economic indicators, eagerly anticipating signs of improvement. Encouragingly, recent upticks in manufacturing activity, reflected in increased new orders and global exports, hint at potential economic revitalization. Continued improvement would certainly bolster our outlook and hope for a more balanced equity market.

However, as we analyze stock market performance over the past year, a glaring observation emerges—the pronounced dominance of technology stocks, leaving other sectors lagging. While such market narrowness historically signals a potential peak rather than a bottom, recent signs of a broadening rally offer hope for a more inclusive market landscape. If sustained, this trend may prompt a rotation out of richly valued tech stocks into other sectors, heralding a more balanced market (as long as the tech bubble doesn’t cause a crash).

In addition to economic indicators, we rely on stock market-driven signals to gauge market sentiment, distinguishing between "risk-on" and "risk-off" environments. Despite lingering recession concerns, current signals favor a "risk-on" stance, indicative of continued upward momentum for stocks.

Nevertheless, a closer examination of short-term technical indicators suggests an overbought market, predisposing it to correction. In anticipation of such market fluctuations and bolstered by signs of a broadening rally and glimmers of positive manufacturing data, we remain poised to increase stock exposure opportunistically while maintaining flexibility with portfolio allocations.

In summary, navigating today's market demands adaptability, patience, and prudence. While we maintain a defensive tilt in portfolio allocations, we stand ready to capitalize on emerging opportunities and adjust our strategy as market conditions evolve. Flexibility remains our guiding principle in seizing opportunities and mitigating risks in this dynamic landscape.

Model Positioning

LHWM portfolio models continue to straddle the possibilities of recession and economic reacceleration through a barbell approach. For the possibility of a recession, a reduced overall weighting to stocks with a focus on defensive and value-oriented equity sectors and a large allocation to short-term and inflation-protected bonds. For the possibility of an economic reacceleration, increased exposure to cyclical sectors and commodity-focused investments.

Short-term treasury notes continue to be the largest portfolio holding. During September and October, proceeds from maturing 12-month notes were used to purchase new 24-month treasury notes with risk-free yield-to-maturities of just over 5%. This was timely as yields dropped over the last few months...the 2-year note yield dropped below 4.15% in December; it has since climbed back up to 4.65% with CPI showing modest reacceleration to 3.1% in January. Stronger inflation data causes rates to move higher because it reduces the chance of rate cuts from the FED. The FED has pledged to hold rates high until they become convinced CPI is heading below 2%.

Portfolio models continue to be underweight equity exposure with holdings focused on defensive and value/dividend-oriented funds. After modestly increasing equity exposure in November/December, we paused on adding additional equity in January as the market rally had gone too far too fast in our view. Models have roughly 50% of the targeted long-term equity exposure. With recent modest improvements in manufacturing data and positive market signals, we anticipate adding some additional equity exposure barring any signal changes.

While we have increased equity exposure and are considering further increases on a dip in the market, we remain with a defensive tilt until the recession indicators clear. The increase in equity exposure is to account for the possibility of the reacceleration scenario. If the FED follows through with a significant easing of monetary policy (they have been pushing back on this idea recently), it could very well unleash a larger rally in stocks (unless rate cuts are a result of something breaking). We expect the market to remain volatile as long as economic growth remains weak and inflation remains high. To navigate this volatility, we will continue to adjust exposures based on macroeconomic and market indicators to reduce portfolio volatility and protect capital. Market risk remains elevated, and we remain cautious.

Keys to the Market

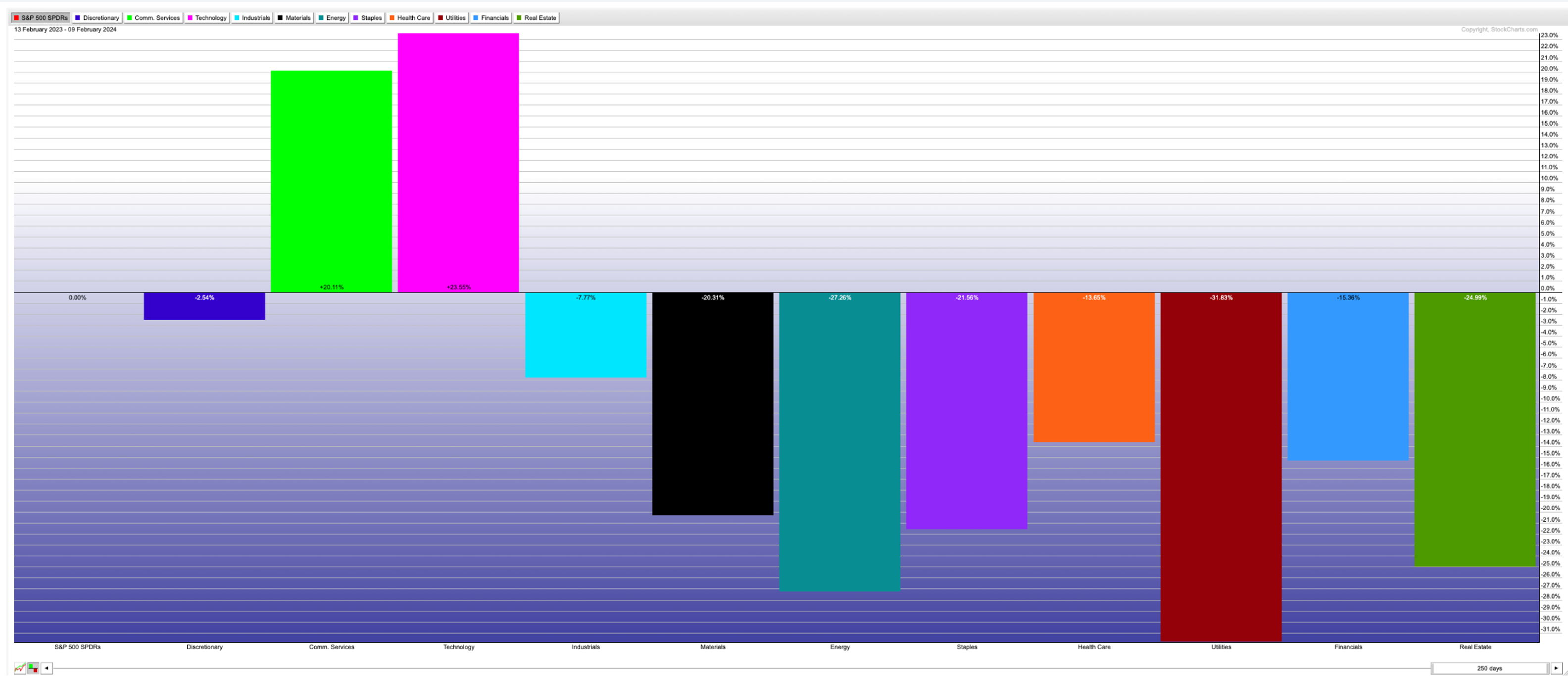

Tech Outperformance – The following charts compare the performance of all 11 sectors in the S&P 500.

Total performance of each sector over the last 12 months. Technology (MSFT, AAPL, NVDA, etc.) and Communication Services (Google & META, etc.)

This chart shows the relative performance of each sector to the S&P 500. Technology and Communication Services have been driving the gains.

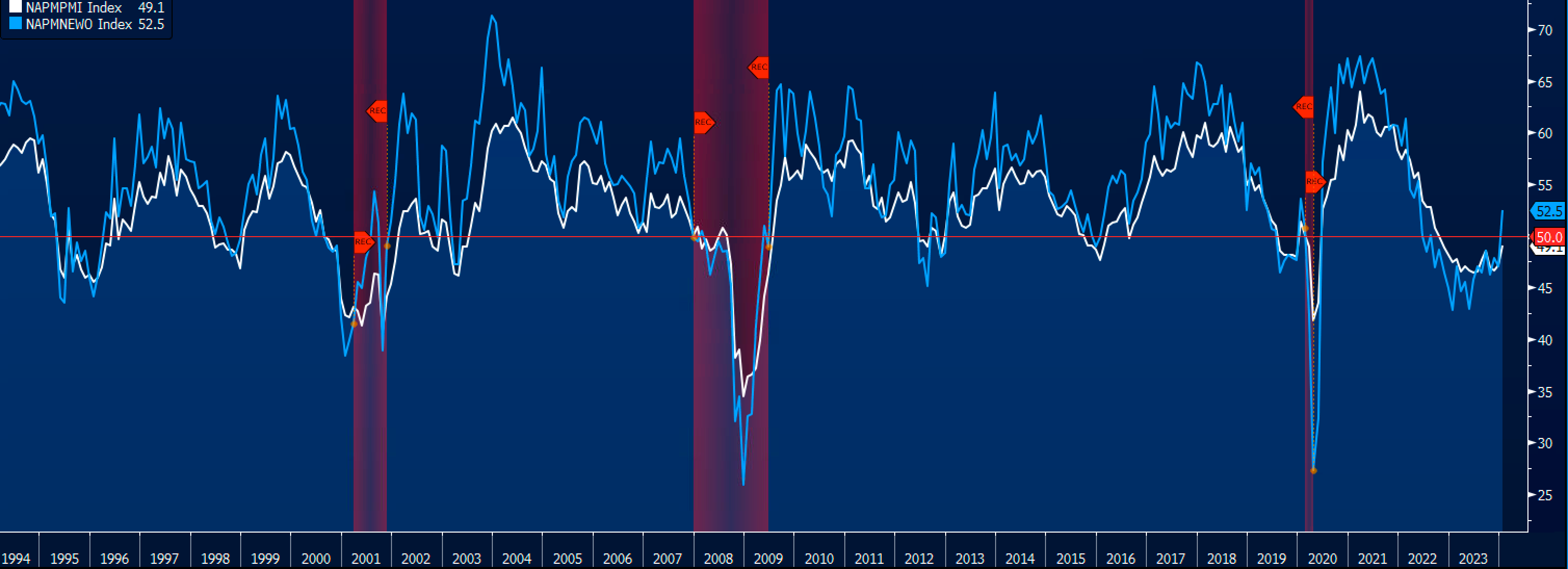

Manufacturing New Orders – Manufacturing new orders have been on the rise (blue line). As can be seen on the chart below, in the past this has predicted an increase in ISM manufacturing PMI (a leading indicator for the economy). Below 50 are indicative of periods of manufacturing contractions.

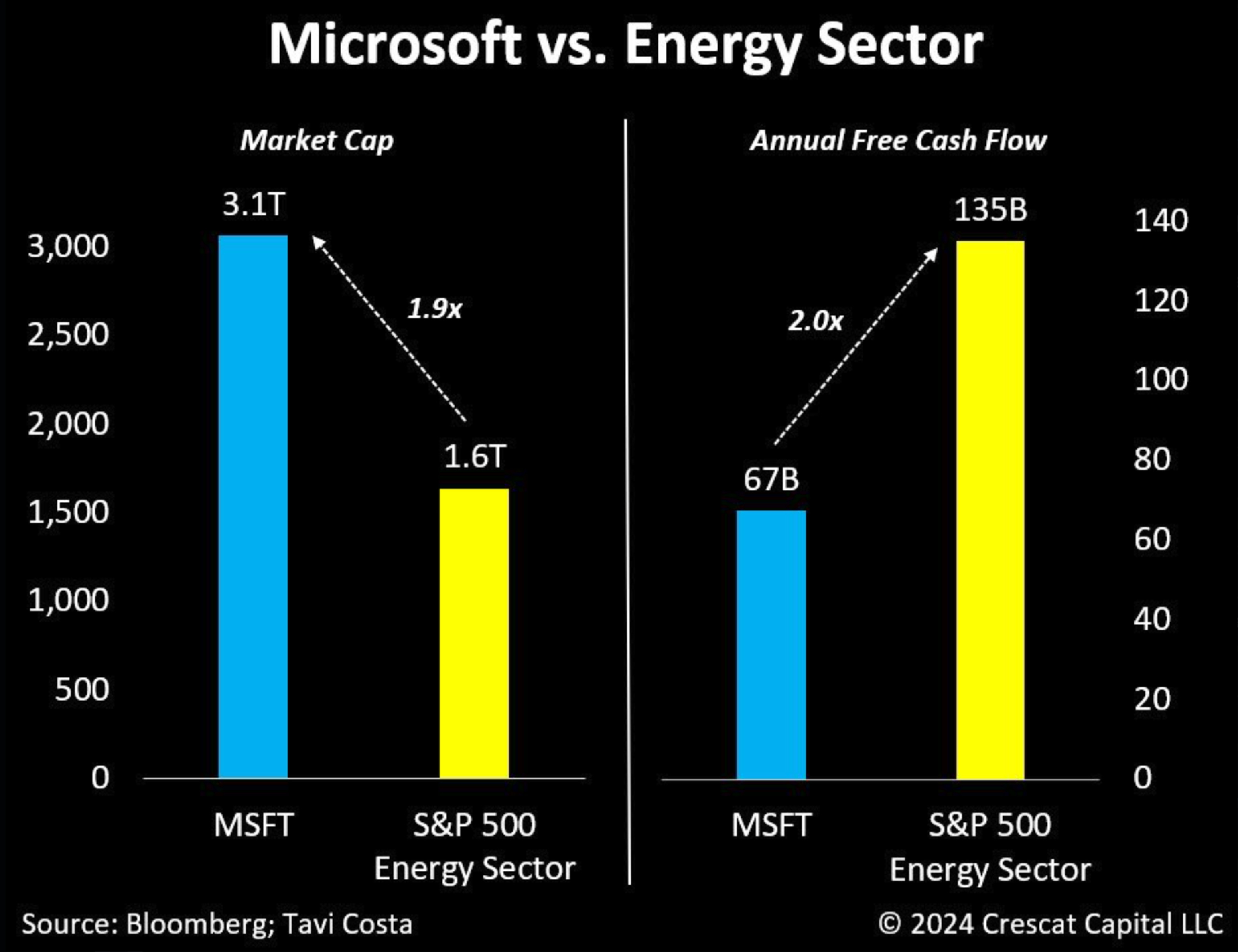

Tech Valuations look frothy – The following chart shows the value of Microsoft is 1.9 times larger than the entire U.S. energy sector. Meanwhile, the annual free cash flow of the U.S. energy sector is 2 times the amount of annual free cash flow for Microsoft.

Bonus Chart: The History of Bubbles- Humans have greatly evolved, yet, we are still greatly influenced by our amygdala, specifically our neverending emotional swings between fear and greed. There are many ways to measure the current greed levels in financial markets, however, the table below illustrates the rise and fall of the most famous bubbles including the current one. Bubbles, during their parabolic run, can be exciting as many participants make a lot of money and believe they have discovered their lottery ticket to fame and riches. However, the fact is, that bubbles eventually pop, reality sets in and the masses lose lots of money as they join the party at the peak. In wealth management, it isn’t what you make, it’s what you keep. There are no shortcuts to lasting wealth and this time is rarely different.

While the stock market remains richly valued and the risk of a global recession remains, LHWM portfolios remain defensively allocated. Our goal is to help you grow your wealth over time while managing the risk of significant drawdowns along the way. Markets never go in a straight line. As we remain defensive, awaiting indication from our technical and economic signals for the time to get bullish, patience is needed. We remain vigilant in navigating these uncertain markets and searching for the start of the next meaningful uptrend. During our relationship, we have worked with you to establish a portfolio that matches your financial planning needs, risk tolerance, and investment timeline. It is critical to remain patiently invested in the appropriate model. Stick to the plan!

Please do not hesitate to contact us with any questions, comments, or to schedule a portfolio review.

Sincerely,

Lake Hills Wealth Management