The Credit Crunch

Key Take Away

The banking crisis that started in March is an ongoing concern. A significant consequence will be a further tightening of credit. In other words, banks will be lending less. It is important to understand that credit growth (debt growth) is a key driver of economic growth. When credit tightens, growth slows or even contracts. We believe this is a much larger issue than the upcoming debt ceiling standoff. Ultimately the debt ceiling will be raised and will likely go down to the last hour. If the U.S. were to experience a technical default by the government, this would mean that payments would ultimately be made late. While not a good scenario in the short term, this debt ceiling crisis will pass. This bigger issue remains continued economic weakness.

With the economy continuing to slow, LHWM models remain very defensive.

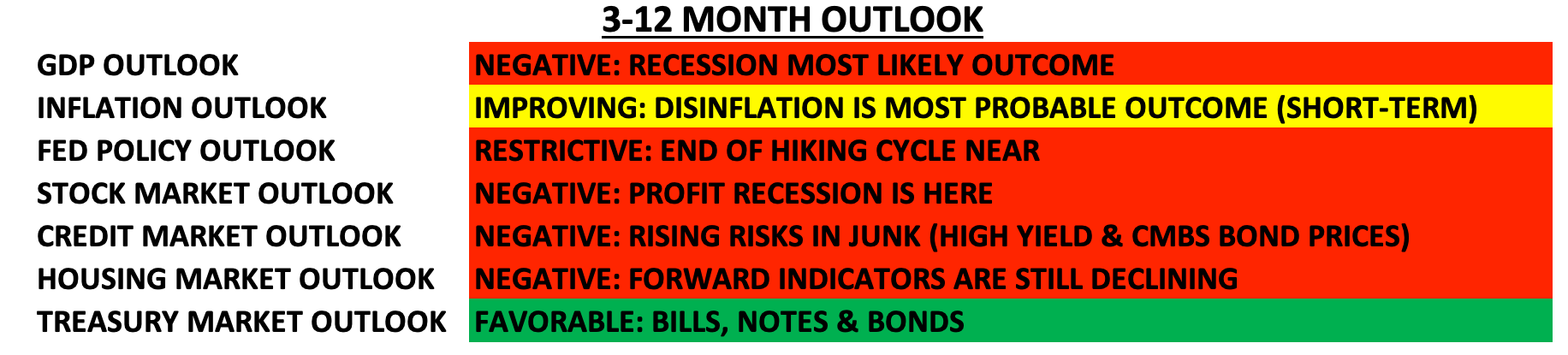

U.S. Outlook (Next 3-12 Months

Overview

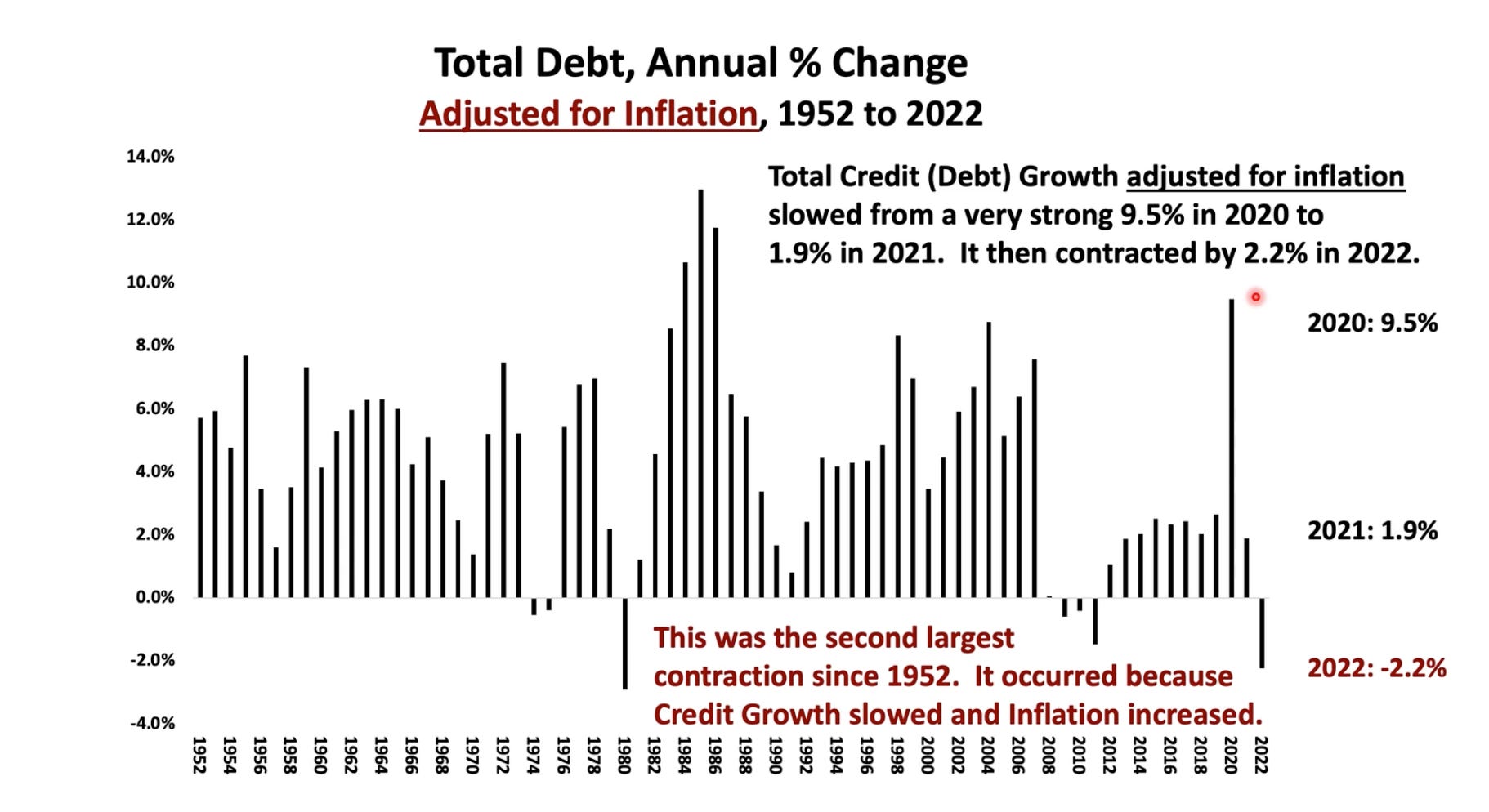

Credit growth (debt growth) is a key component that drives economic growth. Total debt in the U.S. expands just about every year, largely thanks to huge and growing government deficits. In the post-World War II era, until 2009, any time U.S. credit grew by less than an inflation-adjusted 2% rate, the U.S. entered recession (this occurred 9 times). However, after the 2008 financial crisis, this relationship hasn’t held. Households became so indebted in the leadup to the 2008 Financial Crisis that household borrowing materially slowed over the following decade. To pick up this slack, the government took the baton and ramped up borrowing (and spending) to prevent two potential depressions (2008 and 2020). Additionally, the FED became much more active with their Quantitative Easing (“money printing”) policies to prop up asset prices and spur economic growth. QE (Quantitative Easing) worked well to stimulate the economy during the 2009 to 2021 period by driving up asset prices and creating a wealth effect to stimulate spending. They pursued this policy with little issue thanks to a low inflation backdrop. Source: Richard Duncan

As we have previously highlighted, the problem now is that with a high inflation backdrop, the FED cannot aggressively pursue the QE policies of the last 15 years without further stoking inflation. In fact, right now, they are engaged in the opposite policy, QT (Quantitative Tightening). In 2022, when adjusted for inflation, credit growth was -2.2%, the second largest contraction since 1952, behind only 1980. Now that the FED is engaged in QT, credit growth will likely be an important determinant driver for economic growth.

It appears as though the U.S. is in the early stages of a credit crunch due to the banking crisis. Given the two major bank failures in March and other (who knows how many) regional banks facing similar issues (First Republic), deposits have been rapidly leaving these smaller banks. Depositor confidence has been shaken. Additionally, people have been removing deposits from the banking system with higher rates, opting to earn higher yields in short-term treasuries and money market funds. This deposit flight, coupled with the banks’ balance sheet problems, is causing a contraction in the extension of credit. Banks can’t afford to make bad loans, and they have fewer deposits to lend.

Higher interest rates also cause consumers and businesses to borrow less. When borrowing costs increase (especially when inflation-adjusted incomes are negative), people are less inclined to take out a loan. Economic activity slows.

While the squeeze is on households and businesses for access to credit, Congress is also debating what to do about the government budget and debt ceiling with Republican pressure to reduce spending. In recent years, government spending (borrowing) has been a main driver of economic growth (and inflation). Any material cuts to government spending will act as a further decelerate to GDP growth.

The economy continues to decelerate. Real GDP growth in 2021 was 5.9%, with total credit growth of 1.9%; QE policies were at all-time highs this year. In 2022 Real GDP grew by 2.1%, despite a contraction in inflation-adjusted credit growth of -2.2%, likely the economy still fueled by the excess pandemic stimulus QE. So far, in 2023, we have just received the Q1 GDP, which showed an annualized GDP growth rate of 1.1%, proving that economic deceleration is happening. Meanwhile, the economy is slowing, but core inflation remains elevated. PCE (Personal Consumption Expenditures), the FED’s preferred core inflation measure, remains at 4.6%, down from its peak of 5.4% in March of 2022. This is only a gradual reduction in core inflation and will likely prevent the FED from reducing rates anytime soon and will certainly prevent a rush back to QE policies. Source: Richard Duncan

The economic weakness should continue without rate cuts, QE, or fiscal spending in the near term. Corporate earnings have declined over the past year but have held up better than expected as companies continue to increase cost-cutting efforts. We fear that another year of credit contraction, with interest rates higher for longer, will have increasingly more negative economic consequences and ultimately lead to recession. Risk remains high.

Model Positioning

We have not made any material changes to the portfolio over the past month We continue to believe short-term treasury notes (1 year or less to maturity) continue to stand out as an attractive place to park capital in the short term while we await a better, lower, entry point for stock exposure. Additionally, we have accumulated a small position in longer-duration Treasuries bonds as an added portfolio hedge for a recession. The small percentage of stock exposure in all models remains focused on defensive sectors, value, and high dividends.

We expect the market to remain volatile in 2023. To navigate this volatility, we will adjust exposures (long and short) based on our macroeconomic and market indicators to reduce portfolio volatility and protect capital. Market risk remains elevated, and we remain cautious.

Keys to the Market

Total Annual Debt Growth Adjusted for Inflation – In the past (pre-2009), when inflation-adjusted credit growth was less than 2%, the U.S. economy entered a recession 100% of the time until the post-2009 era when the FED began stimulating the economy with QE. However, In 2022, the U.S. saw a -2.2% contraction in credit with no recession, or at least not yet. A recession may have been delayed due to the historic size of fiscal and monetary stimulation as a result of the 2020 COVID-19 pandemic.

*Source: Richard Duncan Economics

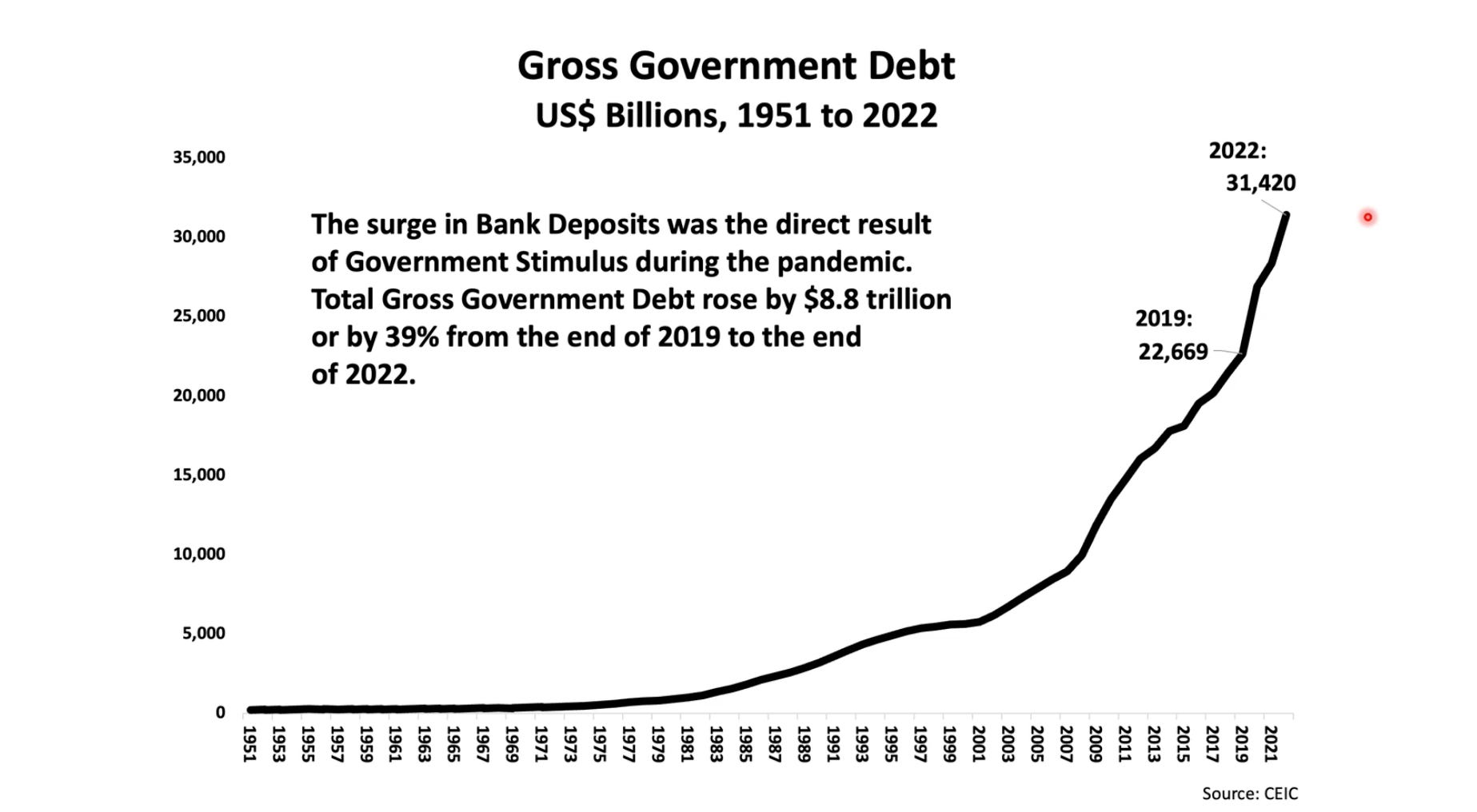

Total Government Debt – U.S. Government debt has surged since the 2008 financial crisis. Government debt has increased by 21 trillion dollars from 2007 to 2022, an increase of 340%. With interest rates increasing, the government’s borrowing cost increases, forcing more of the budget to be allocated to debt service, potentially limiting government spending elsewhere. Debt has increased exponentially while the economy has only grown modestly over the last 15 years.

*Source: Richard Duncan Economics

M2 Money Supply – M2 Money supply (a measure of the aggregate currency held in cash, banks, money markets, and savings deposits) has contracted by over 4% over the last 12 months. This is uncharted territory. We highlighted last month the correlation between M2 growth, economic growth, and stock market performance. What will the lagged effect be of this contraction? Our best guess is it will put negative pressure on asset prices.

*Source: Bloomberg

Markets never go in a straight line. As we remain defensive, awaiting indication from our technical and economic signals for the time to get bullish, patience is needed to ride out the storm. We remain vigilant in navigating these uncertain markets and searching for the start of the next uptrend in the stock market. During the course of our relationship, we have worked with you to establish a portfolio that matches your financial planning needs, risk tolerance, and investment timeline. It is critical to remain patiently invested in the appropriate model. Stick to the plan!

Please do not hesitate to contact us with any questions, comments, or to schedule a portfolio review.

Sincerely,

Lake Hills Wealth Management