The Good, The Bad, & The Ugly

The Good, The Bad, & The Ugly

LHWM Market Quick View-June 2023

Key Take Away

Given the current forward indicators, we believe a Global recession is the most likely outcome, although our recession call has taken longer than expected to materialize. We also recognize the possibility that a U.S. recession may be avoided (although still a low-probability outcome) due to the unprecedented fiscal and monetary stimulus due to the COVID-19 pandemic, the Inflation Reduction Act, and the CHIPS Act. The massive stimulus and government spending have caused significant distortions in the economic data, making economic forecasting much more difficult. We are pursuing a barbell approach with portfolio construction to navigate these dueling possibilities. While tech stocks have enjoyed a nice rally this year, the rest of the market has been left behind and should start to catch up in the event of an economic rebound. For this possibility, we have been buying cyclical stocks (energy, industrials, banks, materials, metals, and miners) which have not participated in the rally (and are still relatively cheap) yet should generate nice gains if the economy rebounds. If the recession plays out, as expected, we will continue to be underweight equity with allocations to defensive sectors on the other end of the portfolio.

U.S. Outlook (Next 3-12 Months)

Overview

The Magnificent 7 (Apple, Amazon, Google, Meta, Microsoft, Nvidia, and Tesla) have continued to lead the market higher, as we highlighted last month, and are very expensive. Yet, economic data and earnings remain lackluster. What gives? A significant disconnect exists between the stock market and the fundamentals (the economy and company earnings). While this disconnect has been frustrating, it is a common phenomenon, especially before a recession. We believe the disconnect will resolve within the next six to eight months either by experiencing a recession (stocks, inflation, and growth declines) or a U.S. economic recovery, leading to higher inflation and interest rates, which could mean a nasty recession during the 2024-2025 timeframe.

Investor pessimism reached extreme levels at the end of 2022, and while the economic data has not been great, the job market and consumer spending have been resilient. On the one hand, U.S. consumers have continued to spend money on travel, experiences, and services even though the cost of living increases have far outpaced inflation adjusted (real) wage gains over the past two years. Consumers have used their “excess savings” accumulated during the pandemic and ran up credit card balances even as interest rates hit record highs to maintain spending. At the same time, corporate America has been in cost-cutting mode to protect profit margins. Like corporate earnings, they have been slowly declining since Q2 of 2022 but have not been as bad as feared (so far). These factors have led to the material rally this year as investors (including Lake Hills) were underweight stocks, leading to another bout of speculation and FOMO (fear of missing out). Maybe the U.S. economic resilience remains, and there won’t be a hard recession as inflation eases, thanks to supply chains easing and slowing demand. Or maybe the recession will be rolling as different sectors of the economy are hit at different times. (Source: Bloomberg)

On the other hand, we continue to have a series of leading economic data warning of impending recession for the U.S. economy. A deeply inverted yield curve for an extended period, rising continuous jobless claims, a manufacturing downturn, and a housing slowdown have all been time-tested indicators for an economic recession. We are coming out of a multi-decade period where spending was fueled with low-interest rates and mountains of government stimulus that drove record profit margins for corporate America. Borrowing costs have since skyrocketed, presenting significant problems for consumers, corporations, and the real estate market. Low-credit quality companies have relied on cheap financing and easy money to remain solvent. So far, the credit market has remained calm despite the large increase in corporate bankruptcies. Until an individual buys a new house or car, they are likely locked in at lower rates on older loans. The same for companies; many raised significant amounts of cash when rates were low, but since most corporate debt matures every five years or so, the longer rates stay high, the worse the problem will be as debt is financed at higher rates. Maybe the unprecedented circumstances around the pandemic have increased the lead time for the recession. The data shows lending growth (credit growth) has been at recessionary levels for around six quarters; however, the recession has most likely been delayed by the excess savings (government stimulus) consumers and companies have stashed away. The restart of student loan payments (3-year deferment ends in September) could be the catalyst that triggers a recession as the consumer spends down the last of their excess cash while credit dries up and real wages (income after inflation) remains negative.

So, either the economy will pick up steam to justify the euphoria of the stock market, or this stock rally will fail as a recession materializes. Which will it be? That is the million-dollar question of the day. While we still believe recession to be the most likely outcome, we also recognize the possibility that the pandemic's echoing effects could distort the economic data and delay the recession further. As a reminder, there has only been one similar time in history to the current: the 1918 Spanish Flu. As you may know, that debt-induced speculative period painfully ended with a series of recessions/depressions during the 1920s that ultimately led to the Great Depression of 1929. Mark Twain once said, “History doesn’t repeat itself, but it often rhymes,” so being vigilant yet open-minded is critical.

Model Positioning

We have been pursuing a barbell approach to portfolio construction to account for the possibility of a recession and a soft landing (no recession). Part of the portfolio continues to be prepared for recession with exposure to short-term treasury notes, allocations to defensive sectors, inverse equities, and overall underweight equity exposure. To account for the possibility of a soft landing, we have continued to add to cyclical stock exposures that are still at relatively low valuations and tend to do well in periods of high inflation. Overall, the portfolio models remain defensive, so if the stock market continues to go up, we will lag our benchmark.

We expect the market to become more volatile in the back half of 2023. To navigate this volatility and confusing time, we will continue to adjust portfolio exposures based on our macroeconomic and market indicators. As a reminder, our strategy uses data-driven indicators to add or subtract risk depending on the reading of those indicators. The goal is to make money, but when these indicators flash red (caution), the overarching goal shifts to reduce risk and portfolio volatility while increasing more reliable income streams and, more importantly, protecting capital. Market and economic risks remain elevated, and thus we remain cautious.

Keys to the Market

The Good

Year-to-Date S&P 500 Total Return: So far, the year-to-date return for the S&P 500 has been spectacular. As of the end of the quarter, the S&P 500 reached 4450, which is about 8.5% above the median Wall Street analyst year-end price target. This sounds great; however, after further analysis, we found that 73% of the year-to-date return is attributable to 7 stocks, commonly referred to as the magnificent 7 (Apple, Microsoft, Nvidia, Amazon, Telsa, Meta, and Google). We should also point out that most of the Magnificent 7 stocks have declining earnings and have been feverously bid up on the release of some new AI (Artificial Intelligence) technology and chips. While AI is revolutionary, it isn’t new or being monetized, meaning most companies aren’t profiting from it at this time. The reaction to AI looks much like the internet craze of the 90s, which eventually led to the dot-com bubble and subsequent crash. The Internet did change the world but had you bought into the tech stocks of that era; you would have experienced massive losses, which took many a decade or more to recover. The price you pay does eventually matter.

Even though there is narrow leadership in the market, increasing stock prices usually make consumers, economists, and strategists feel better about spending, the economy, and markets. The chart below shows the year-to-date return for the S&P 500.

Source: Bloomberg

The next chart shows the return of the S&P 500 and the return of 1-3 month Treasury bills from January 1, 2022 (the beginning of the bear market) to June 30, 2023. As you can see (click the image), 1-3 month Treasury bills have outperformed the S&P 500 with much less risk and volatility. Perspective and patience are key during economic contractions and bear markets.

Source: Bloomberg

The Bad

Excess Savings –This chart shows personal savings spiked during the pandemic. A massive buildup of savings thanks to the combination of unprecedented government stimulus and people staying home during the early stages of COVID-19. As the economy reopened and inflation surged, personal savings have dropped sharply. The lower panel shows the estimated accumulated excess savings, rapidly dwindling. For the average American, inflation is a thief as real wages (wages after inflation) are negative, and savings must be used to maintain their lifestyle or, in some cases, the bare necessities. As mentioned above, Student loan payments have been in deferment since the pandemic's beginning, but that deferment is ending. Starting October 1, student loan payments will go back into repayment with interest beginning in September. According to the New York Fed, the outstanding student loan balances are $1.6 Trillion, with an estimated monthly household payment of $250. Obviously, this has been a big reason for high consumer spending and inflation; however, assuming most student loans go back into repayment, the drag on retail sales could be around 0.5-1% which is quite large. This alone could be the catalyst that sends the U.S. into a recession. Time will tell…

Source: Ned Davis Research

The Ugly

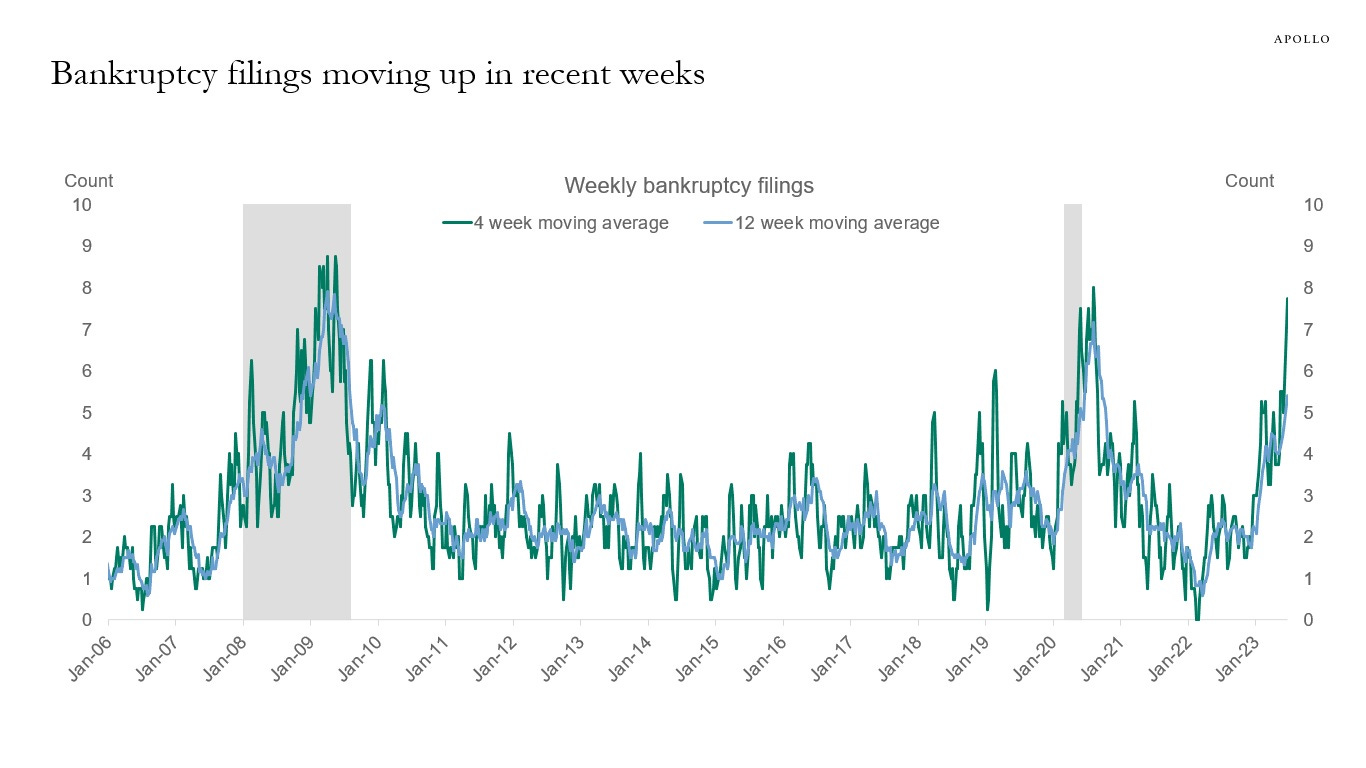

Business Bankruptcies –According to the Federal Reserve, the balance of business debt is just under $20 Trillion (as of March 31, 2023), which has grown by around 17% since the beginning of the pandemic. As we have discussed before, The Fed has increased the Fed Fund rate 10 times since March of 2022. This action by the Fed has caused the average financing rate for corporations to rise from around 2.5% to over 5%. This is an average, so many higher credit-risk companies pay much higher rates than the average. The rapid increase in financing rates has not only slowed borrowing but has started to create casualties in the business world. The chart below illustrates the number (4 & 12-week moving average) of business bankruptcy filings in the U.S. As the economy slows, lending stalls, and the cost of capital increases, so has the weekly filings of business bankruptcies. While we’re not currently seeing the same level of systemic risk that occurred in the Great Financial Crisis of 2008-2009, things are rapidly changing. The longer the Fed fights inflation with higher rates and Quantitative Tightening (removing liquidity), the worse the credit picture gets for businesses and consumers.

Source: Apollo

We aim to help you grow your wealth over time while managing the risk of significant drawdowns. Markets never go in a straight line. As we remain defensive, awaiting indication from our technical and economic signals for the time to get bullish, patience is needed to ride out the storm. We remain vigilant in navigating these uncertain markets and searching for the start of the next meaningful uptrend in the stock market. During the course of our relationship, we have worked with you to establish a portfolio that matches your financial planning needs, risk tolerance, and investment timeline. It is critical to remain patiently invested in the appropriate model. Stick to the plan!

Please do not hesitate to contact us with any questions, comments, or to schedule a portfolio review.

Sincerely,

Lake Hills Wealth Management