Tug of War

Key Take Away

The recent FED pivot talk has sparked a rally in the stock and bond markets while the U.S. dollar and commodities have declined. While the FED has not cut rates, they have allowed the market to believe there will be no further rate hikes and that rates will be cut in 2024. Thus, traders have immediately pushed interest rates lower, effectively pricing in significant rate cuts as if they have already happened. The market could be a little ahead of itself. Generally, the FED moves slowly unless forced by a crisis such as a weak economy/recession, a stock market crash, or when something breaks in the financial system. This unexpected FED pivot has added fuel to the market pendulum swinging from oversold conditions at the end of October to over-bought conditions at the end of December. The animal spirits are definitely on full display.

Over the last month or so, we have added equity exposure to models to account for the possibility of a soft landing with this shift in the FED policy outlook. After all, no sitting president (Republican or Democratic) wants to see a recession on their watch, especially if they seek reelection. Right or wrong, the FED is now thinking about cutting rates, which has excited the stock market. In the past, rate cuts have more often than not coincided with recessions and declining stock prices. Hopefully, this time will be different. We remain cautious but flexible if the data and indicators warrant a change on our part. Overall, we believe 2024 will be a make-or-break year, as many current recession indicators will be invalid if a recession doesn’t materialize in 2024.

Last month, we mentioned that the Treasury had surprised the market by adjusting its funding plans to use more short-term rather than long-term debt. This took the pressure off long-term rates and sparked a rally. Now, the FED just added fuel to the rally with their pivot talk, and if interest rates stay at the current range (below 4% 10-year treasury), it will stimulate the economy and could reignite inflation. In the short term, the market is over-extended and has run too far too fast. Fundamentally, to keep the rally in stocks going, we must see improved earnings and above-trend economic growth while subduing rates and inflation. Many positive outcomes have already been priced in the stock and bond market, and this could be a headwind in early 2024, recession or not.

For now, portfolios remain defensive as we watch to see if the economy can gather steam (global manufacturing), see the treasury funding announcement for the first quarter, and find out how serious the FED is about easing monetary policy.

U.S. Outlook (Next 3-12 Months)

Overview

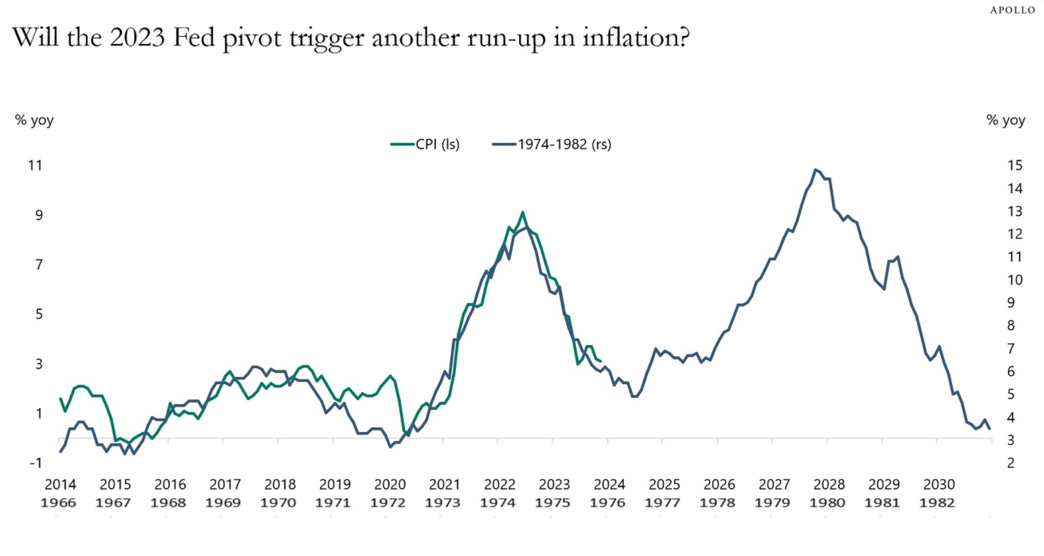

Stocks and bonds finished 2023 with a significant rally as the FED’s surprise pivot on December 13th unleashed a stampede of buying. The pivot was a surprise insofar as just two weeks earlier, on December 1st, Fed Chairman Powell had said, “It would be premature to conclude with confidence that we have achieved a sufficiently restrictive stance, or to speculate on when policy might ease.” The chairman had spent the better part of the last year stressing the importance of keeping rates restrictive enough to bring inflation down to their stated target of 2% and how deviating from the battle on inflation too soon was the greatest risk they faced. If they were to pivot and ease too soon, without inflation having been sufficiently squashed, a resurgence in inflation could emerge as it did in the 1970s (see charts below).

To be clear, the FED has not officially said they are cutting rates. However, Powell did not push back on the market’s expectation for rate cuts in 2024; he essentially indicated that cuts are coming. The market took the cue and was off to the races. Bond market participants are now pricing in about six rate cuts (a reduction of about 1.5% in short-term rates) in 2024. Meanwhile, the FED Dot Plot (a culmination of rate expectations among FED members) shows only three rate cuts next year. Powell gave an inch, and the market took a mile. This could mean that the market has gotten ahead of itself with the bond and stock rally, and we could see rates inching back up to align with the FED projections. Or maybe the FED is underestimating how much they will be cutting rates next year. It’s a tug-of-war between a soft landing and recession, with the soft landing (or no landing) narrative having the market momentum for now.

Inflation has steadily declined over the past year but remains well above the Fed’s 2% target. October CPI (released in November) came in at 3.2% yoy (year on year), and November CPI (released in December) was 3.1% yoy. Never mind the changes to CPI calculations (i.e., health insurance, etc.) to help paint a softer inflation picture. CPI is a made-up number anyway…a basket of goods and services that they change from time to time. The real question is: has inflation been sufficiently beaten and contained? Only time will tell. Investors have been anxiously awaiting a pivot from the Fed to ease financial conditions. Then, by Powell simply not pushing back on market expectations, we have now experienced a significant easing in financial conditions; the equivalent of 6 rate cuts is already priced into the market. If these cuts don’t occur, it will essentially be a re-tightening of policy. What if inflation remains stubborn? During the two weeks between December 1st, when Powell said it was premature to consider cuts, and December 13th, when he refrained from pushing back on cuts, most of the economic data points released during this period came in with a slightly hawkish tilt (giving little indication of inflation easing further). What changed to provoke this pivot?

One factor that could be contributing to the FED’s pivot is the recent weakness in the FED Beige Book, which gives a read on the economic status of the 12 Fed districts. Most of the districts gave readings of slowing growth or slight contractions. Also, PPI (Producer Price Index), a measure of inflation on input costs for goods and services, came in at -0.9% yoy for November 2023. PPI tends to lead CPI. So, barring a resurgence in PPI, maybe CPI does continue to fall. The market remains hopeful that inflation will continue to come down, allowing the FED to cut interest rates, all while the economy continues to grow. As a reminder, a soft landing (no recession) has only happened 20% of the time with prior rate hiking cycles, with the last one in 1995. Looking at 1995, the current conditions do not look like they did then, so we remain skeptical of this analog. This time could be different (no recession), but historically, uttering such a phrase has been detrimental to one’s portfolio value.

The Fed generally prefers to move slowly. Gradual rate increases, then pause and observe for a while, eventually followed by gradual rate cuts to ease conditions slowly. Rapid policy changes generally require economic or financial plumbing issues to force their hand. With the market currently pricing in six-plus rate cuts next year, this would be more akin to periods of economic turmoil forcing the FED to move quickly. The FED Dot Plot showing three rate cuts is more in line with a gradual rate-cutting cycle commencing. It seems that either stocks or bonds are incorrectly pricing the future. If corporate earnings accelerate from here and the economy reaccelerates, as the stock market is seemingly predicting, rapid rate cuts will not be needed. On the other hand, if a rapid rate-cutting cycle ensues, as the bond market is predicting, it will likely be due to economic weakness forcing the Fed to cut rates quickly. If the bond and stock markets accurately price the future, we are headed for more uncharted territory. We believe the most probable outcomes are a recession or a resurgence of inflation, which could spark much more volatility for stocks and bonds next year.

We remain patient with a defensive tilt, waiting for data and indicators to provide a fundamental reason to be more bullish. We are watching for improvements in the Leading Economic Index, signs of sustained lower inflation (and thus interest rates), and acceleration in global manufacturing. When these things begin to show improvement, this could cause us to increase equity exposure, assuming our market indicators are still constructive. Additionally, we’ll continue to monitor the FED to see if they provide further indication of their plans to ease policy. No matter how this cycle ends, we believe the next ten years will likely NOT look like the last ten years. Opportunities to make money will come. However, we believe interest rates and inflation will be more volatile in the coming decade, thus creating more volatility in the financial markets. Being data-dependent, humble, patient, and flexible will be the key to success in the future.

Model Positioning

Short-term treasury notes continue to be the largest portfolio holding. During September and October, we used proceeds from maturing 12-month notes to purchase new 24-month notes with yields of just over 5%. This has proven to be a good move as yields have plunged over the last few weeks, with the 2-year note yield now down around 4.25%.

Portfolio models continue to be underweight equity exposure, with holdings in defensive value/dividend-oriented funds. However, we have added some equity exposure over the last month with our focus on the lagging areas of the equity market. China, emerging markets, and green energy stocks are a few areas that look particularly interesting from our perspective. China is trading at levels seen during the 2008/09 recession, offering significant upside on a recovery. We are also looking at other cyclical and commodity-focused investments. Growth and technology stocks are already pricing in a rebound; we expect these areas to underperform while the rest of the market plays catch up if an economic reacceleration ensues.

While we have increased equity exposure, we remain defensive until Leading Economic Indicators improve and corporate earnings accelerate. The increase in equity exposure accounts for the possibility of a soft landing/or no landing scenario. If the FED follows through with a significant monetary policy easing, it could unleash a larger stock rally. We expect the market to remain volatile as long as economic growth remains weak and inflation remains high. To navigate this volatility, we will continue to adjust exposures based on macroeconomic and market indicators to reduce portfolio volatility and protect capital. Market risk remains elevated, and we remain cautious as the risk/reward for most developed stock markets is poor, at least from a fundamental standpoint (earnings, real rates, and valuations).

Keys to the Market

Inflation – As measured by CPI, inflation has steadily fallen since the summer of 2022. The FED has warned that ending the fight against inflation too early would risk seeing a resurgence in inflation. The chart below compares today’s inflation path to inflation during the 1970s. With the FED indicating that a pivot in policy is on the way, it begs the question: Will the 2023 FED pivot trigger another inflation run-up?

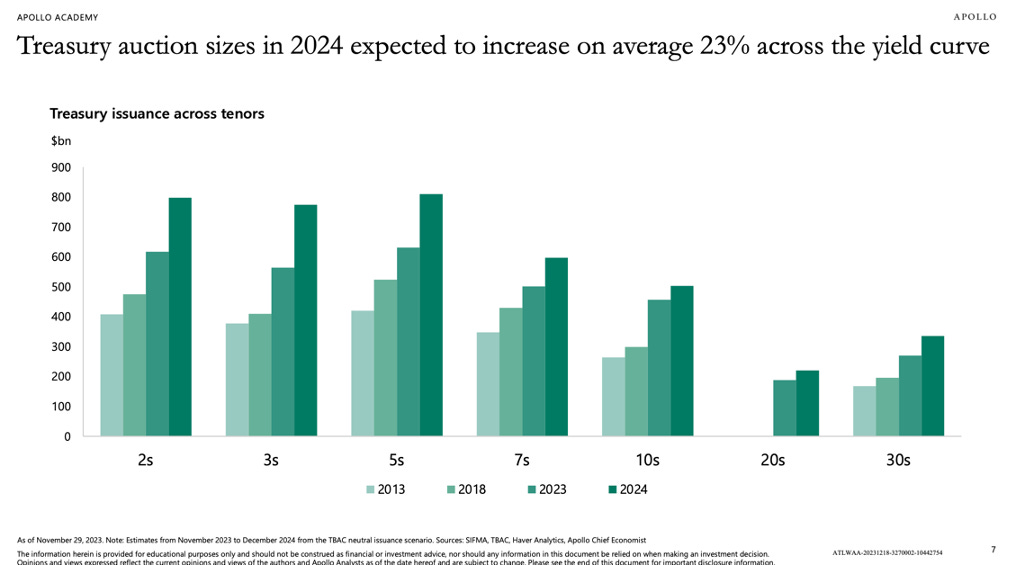

Treasury Auction Sizes – Interest rates may not go down quietly during 2024. Treasury auction sizes are expected to increase on average 23% year over year across the yield curve during 2024. This is due to the amount of government debt maturing (that needs to be refinanced) and the amounts needed to fund the 2024 deficit. The total needed could be $8 Trillion or more. This increased need for capital by the U.S. Government will apply continued pressure on rates to remain elevated unless a marginal buyer steps in. Large deficit spending has also led to inflation in the past.

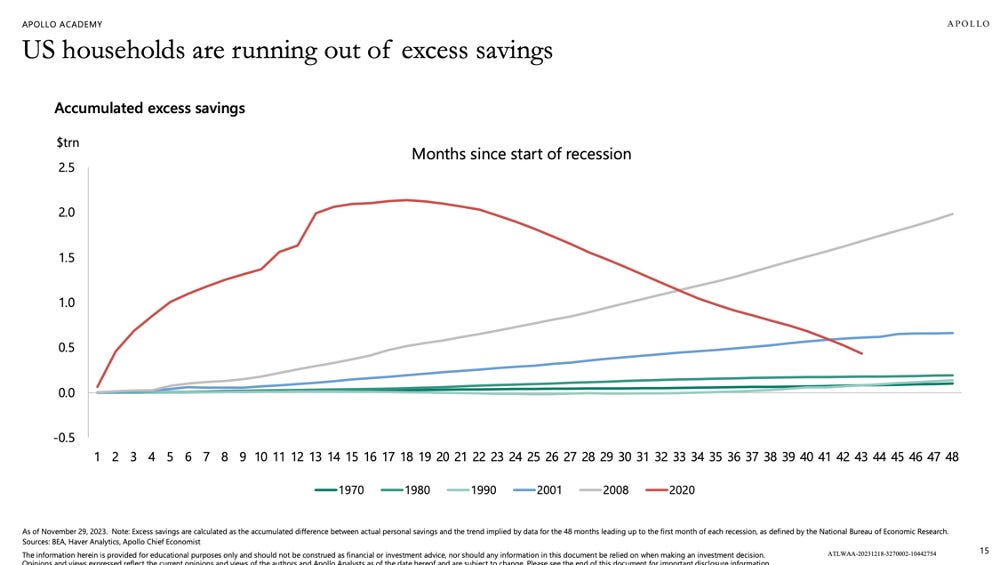

Excess Household Savings – Excess household savings, which got a boost from the post-covid stimulus, continue to decline. This suggests that consumer households may soon have to tighten spending budgets. If consumers reduce spending, this would be recessionary and could apply deflationary pressures on CPI, as money supply and bank lending have been forecasting for most of 2023.

Corporate Earnings Expectations – Meanwhile, corporate earnings expectations have been creeping higher. The bar has been raised, making it more challenging for companies to have positive earnings surprises (i.e., materially beat what is already priced in and expected by the analyst community).

While the stock market remains richly valued and the risk of recession remains, LHWM portfolios remain defensively allocated. Our goal is to help you grow your wealth over time while managing the risk of significant drawdowns along the way. Markets never go in a straight line. As we remain defensive, awaiting indication from our technical and economic signals for the time to get bullish, patience is needed. We remain vigilant in navigating these uncertain markets and searching for the start of the next meaningful uptrend. During our relationship, we have worked with you to establish a portfolio that matches your financial planning needs, risk tolerance, and investment timeline. It is critical to remain patiently invested in the appropriate model. Stick to the plan!

Please do not hesitate to contact us with any questions, comments, or to schedule a portfolio review.

Sincerely,

Lake Hills Wealth Management