Wile E. Coyote vs the Road Runner

Wile E. Coyote vs the Road Runner

LHWM Market Quick View-July 2023

Key Take Away

Leading economic indicators continue to flash warning signs for a weakening economy. While the recession has not yet developed, corporate profits have declined by about 9.76% from the Q1 2022 peak (the current earning season hasn’t concluded). Given the exuberance in the stock market and weak leading economic indicators, conditions are ripe for an accident. Just like tornados or hurricanes, we receive early warnings when conditions are present for these life-threatening storms, at which time we prepare for danger while remaining hopeful for the best outcome possible. The same is true for the stock market and the economy. Today, leading indicators still suggest a global recession is the most probable outcome (a deep recession at that) and a stock market downturn. We remain hopeful that economic winter doesn’t happen, but until our indicators change, we must stay defensive until the storm passes.

Lake Hills models remain defensively positioned while pursuing a barbell approach with portfolio construction to navigate the dueling possibilities of a recession and soft landing (no recession). For the possibility of a soft landing, we have been buying some cyclical stocks (energy, industrials, financials, materials, metals, and miners), which have lagged this year’s rally in growth stocks (and are still relatively cheap), yet should generate nice gains if the economy rebounds. If the recession plays out, as expected, we will continue to be underweight equity with allocations to defensive sectors and short-term treasury bills and notes.

Overview

Many of us grew up watching Wile E. Coyote try in vain to catch the Road Runner. Rather than using traditional methods and instincts, the coyote would rely on some outlandish contraption to capture the Road Runner. These contraptions would comically fail every time to the peril of the coyote. In many ways, today's stock market participants remind us of these timeless cartoons with investors playing the part of the coyote. Each episode would feature a moment where it appears the coyote is about to catch the Road Runner, when suddenly the tables turn, and the coyote finds that he has run off the edge of a cliff (or something to that effect). The coyote would become so consumed with catching the Road Runner that he would pay no attention to his surroundings and wouldn’t realize he was in danger until it was too late.

Lesson: just because you CAN run fast doesn’t always mean you SHOULD. Just like the Roadrunner, we believe pausing and seeing what lies ahead is wise.

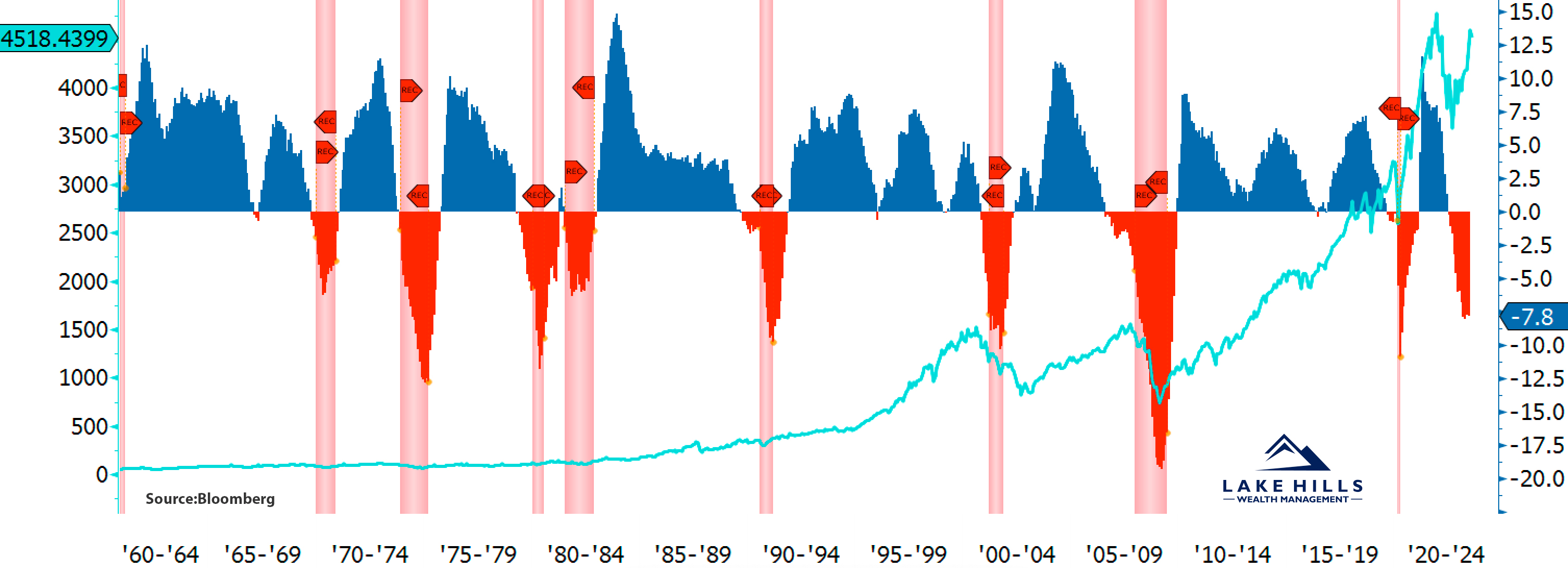

Regarding the economy and the stock market, we’ve been relentlessly pointing out the many economic warning signs over the past year. Although we’ve been wrong so far, these warning signs remain in cautionary territory. Lately, it seems investors have brushed those warnings aside and decided this time must be different. Similar to behaviors exhibited by investors before the last two recessions, 1999-2000 & 2007/08. The most encompassing leading indicator for the economy would be The Conference Board’s LEI (Leading Economic Index) which comprises ten leading economic components. The LEI is currently negative and has been giving negative readings for 15 consecutive months (chart below). This is the longest streak of negative readings since the 2007-09 recession. The LEI is designed to provide an early indication of significant turning points in the business cycle and where the economy is heading in the near term. The exact timing of a recession is always a challenge, and since these are leading indicators, the LEI can be negative for a while before a recession finally hits. For example, the LEI was negative for 15 consecutive months before the start of the 2007-09 Great Recession…so looking back, warning signs were present for those paying attention. Like now, investors became impatient and started believing the soft-landing (no recession) narrative as the recession didn’t develop immediately. So far, the only variable that has changed has been stock prices, and that alone often creates an ill-timed speculative frenzy driven by greed and FOMO (Fear of Missing Out). We could be witnessing Wile E. Coyote running straight off the cliff… Beep beep! Source: Bloomberg

To further our concerns, we continue to see indications of a weakening consumer. The U.S. economy is roughly 70% consumer based. In other words, consumer spending is the main driver of real economic growth. If consumers slow down spending, the economy goes into recession. We’ve seen negative real wage growth over the last two years (cost of living increasing faster than income). Real retail sales (which are adjusted for inflation) are in contraction when viewed on a 12 and 24-month basis. Nominal sales are up, but when adjusted for inflation, consumption has been headed lower, and they haven’t even started repaying their student loans (payments begin in October). High-interest rates and inflation are undoubtedly a burden for the average American household. Source: Bloomberg

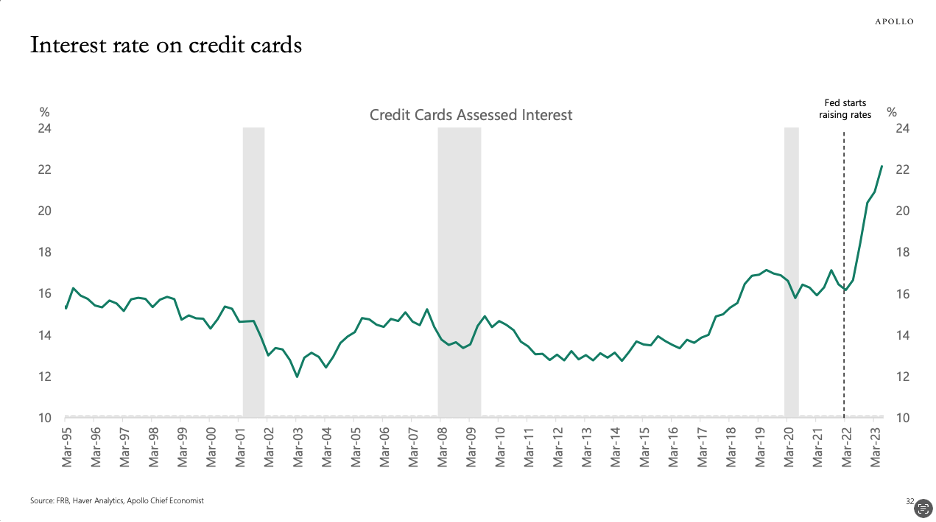

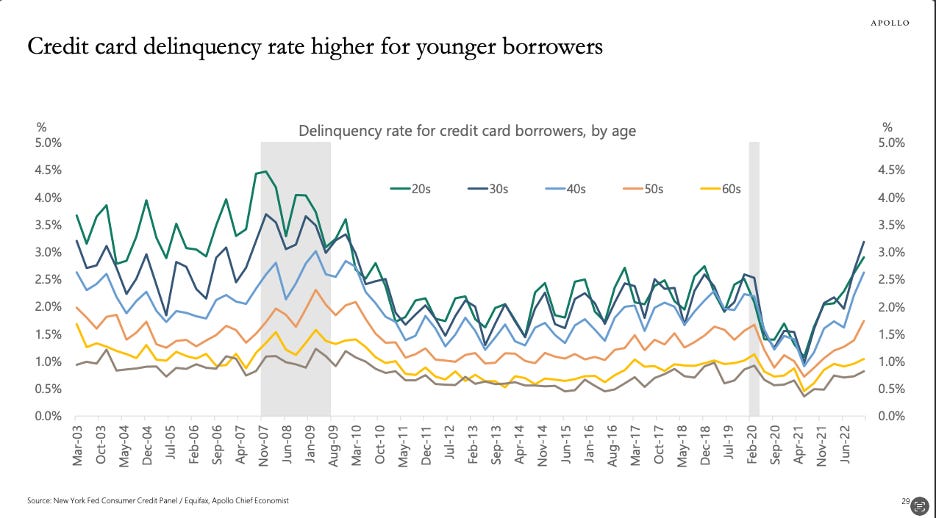

Another sign of a weakening consumer can be found by looking at credit card and other consumer debt delinquencies. Credit card debt is currently over 1 trillion and has risen 33% since March of 2021, while credit card interest rates in the United States are also at all-time highs. The average rate is now in excess of 22%! How long can that go on? Financing anything at a +20% rate will result in consumers paying over double the cost of goods purchased if the debt is carried out for five years. Meanwhile, credit card delinquencies have been climbing (see chart below)…a sign that consumers are stressed trying to make ends meet. Source: Bloomberg

High-interest rates are also playing a hand in the recent uptick in Corporate bankruptcies, which have been accelerating this year, with 340 U.S. firms filing for bankruptcy in the first half. Meanwhile, the Fed has continued to hike rates and has pledged to keep rates higher for longer. Companies that need to borrow have been holding off on refinancing in hopes of lower rates. Over 40% of the Russell 2000 small-cap index companies are currently unprofitable. Source: Bloomberg

But, but, but…the economy isn’t doing that bad because the labor market is still strong, right? Right? Well…employment is a lagging indicator, so it's generally too late by the time this starts to give negative readings. For the month of July, the economy added 187,000 non-farm jobs. That was the headline. It sounds great on the surface; however, if we look under the hood at U.S. total employment for July, the economy added 972,000 part-time jobs while losing 585,000 full-time jobs (credit: Liz Ann Sonders, Chief Investment Strategist at Schwab).

So why are investors ignoring the warning signs? Consumers are struggling to make ends meet, especially younger and lower-paid cohorts. The LEI has been negative for a while now, and the recession hasn’t developed yet. People begin to believe this time must be different (history repeats), and maybe there won’t be a recession. History would suggest this behavior is par for the course. Investors keep chasing stocks just like the coyote chases the road runner, paying no attention to the many warning signs. Then, just like when the coyote discovers he has run off the cliff, greedy or complacent investors may find themselves holding the bag, unknowingly plunged off the economic cliff, only to discover they paid a premium for stocks that were priced for economic growth, not a recession.

Model Positioning

We have continued to pursue a barbell approach with portfolio construction to account for the possibilities of a recession and soft landing (no recession). On the one hand, the portfolio remains prepared for recession with a reduced overall exposure to equities, defensive sector exposures, inverse equities (for hedging), and significant exposure to short-term treasury notes. On the other hand, for the possibility of a soft landing, we have continued to add to cyclical stock exposures that are still at relatively low valuations, which should have significant upside potential if the economy reaccelerates. Overall, portfolio models remain defensive.

We expect the market to remain susceptible to bouts of volatility as long as economic growth remains weak. To navigate this volatility, we will adjust exposures (long and short) based on macroeconomic and market indicators to reduce portfolio volatility and protect capital. Market and economic risk remain elevated, which keeps our client portfolios tilted defensively.

Keys to the Market

Leading Economic Index – The following commentary is from the Conference Board: “The US LEI fell again in June, fueled by gloomier consumer expectations, weaker new orders, an increased number of initial claims for unemployment, and a reduction in housing construction,” said Justyna Zabinska-La Monica, Senior Manager, Business Cycle Indicators, at The Conference Board. “The Leading Index has been in decline for fifteen months—the longest streak of consecutive decreases since 2007-08, during the runup to the Great Recession. Taken together, June’s data suggests economic activity will continue to decelerate in the months ahead. We forecast that the US economy is likely to be in recession from Q3 2023 to Q1 2024. Elevated prices, tighter monetary policy, harder-to-get credit, and reduced government spending are poised to dampen economic growth further.”

https://www.conference-board.org/topics/us-leading-indicators

Real Retail Sales – The consumer has been weakening, with Real retail sales in contraction on a 12 and 24-month basis. To make matters worse, student loan payments are set to resume in October, which will likely further reduce consumer discretionary spending. “There are a total of 45 million people with student loans, and the average monthly student loan payment is around $200. So resuming student loan payments in October will subtract roughly $9 billion from consumer spending every month, or roughly $100 billion a year, and this will mainly have an impact on younger households.” – Torsten Slok, Apollo

Credit cards – Credit card interest rates are at an all-time high, currently above 22%. Even in the 1980s, when rates and inflation were high, the average rate on credit cards topped out around 17%. Not surprisingly, credit card delinquency rates have been climbing, especially for younger borrowers.

The most probable outcome remains a global recession, but the exact timing of a recession is always tricky. Given the elevated probability of a U.S. recession coupled with historic stock valuations, the $46 trillion dollar question remains; how far will stocks fall, especially those in the technology and semiconductor sectors?

We are determined to help you navigate this uncertain economic environment with our eyes steadily focused on the warning signs around us. Our goal is to help you grow your wealth over time while managing the risk of significant drawdowns along the way. Markets never go in a straight line. As we remain defensive, awaiting indication from our technical and economic signals for the time to get bullish, patience is needed to ride out the storm. We remain vigilant in navigating these uncertain markets and searching for the start of the next meaningful uptrend in the stock market. During the course of our relationship, we have worked with you to establish a portfolio that matches your financial planning needs, risk tolerance, and investment timeline. It is critical to remain patiently invested in the appropriate model. Stick to the plan!

Please do not hesitate to contact us with any questions, comments, or to schedule a portfolio review.

Sincerely,

Lake Hills Wealth Management